Kotlikoff Discusses Proposals for U.S. Banking Overhaul: Video

the whole system is corrupt … told by Laurence Kotlikoff

Kotlikoff Says Banks Should Operate Same as Mutual Funds: Video

Larry Kotlikoff: Why I Support Sovereign Money

Larry Kotlikoff on the Clash of Generations

‘US hides real debt, in worse shape than Greece’

The 2008 Financial Crisis: Crash Course Economics #12

The Last Days Of Lehman Brothers Moral Hazard 2008

Global Financial Meltdown – One Of The Best Financial Crisis Documentary Films

Crash Begins! PETER SCHIFF (DEC 2018) Economic Collapse Of U.S on 2018. Timeline to Dollar Collapse

Peter Schiff: The markets are going to collapse due to Fed raising rates

Ep. 428: The Fed’s Deal with the Devil

Why the Worst Market Crash EVER Will Happen in 2018

Debt bomb: Are we on the brink of another global financial crisis?

EXCLUSIVE!! JIM ROGERS EXPLAINS HOW BAD THE DEPRESSION WILL BE AND THE TRADE WAR WITH CHINA!

Alert! JIM ROGERS: The economic collapse will occur 100% / Last warning for December, 2018

Will there be a recession in 2019?

How Did America Go Bankrupt? Slowly, At First, Then All At Once!

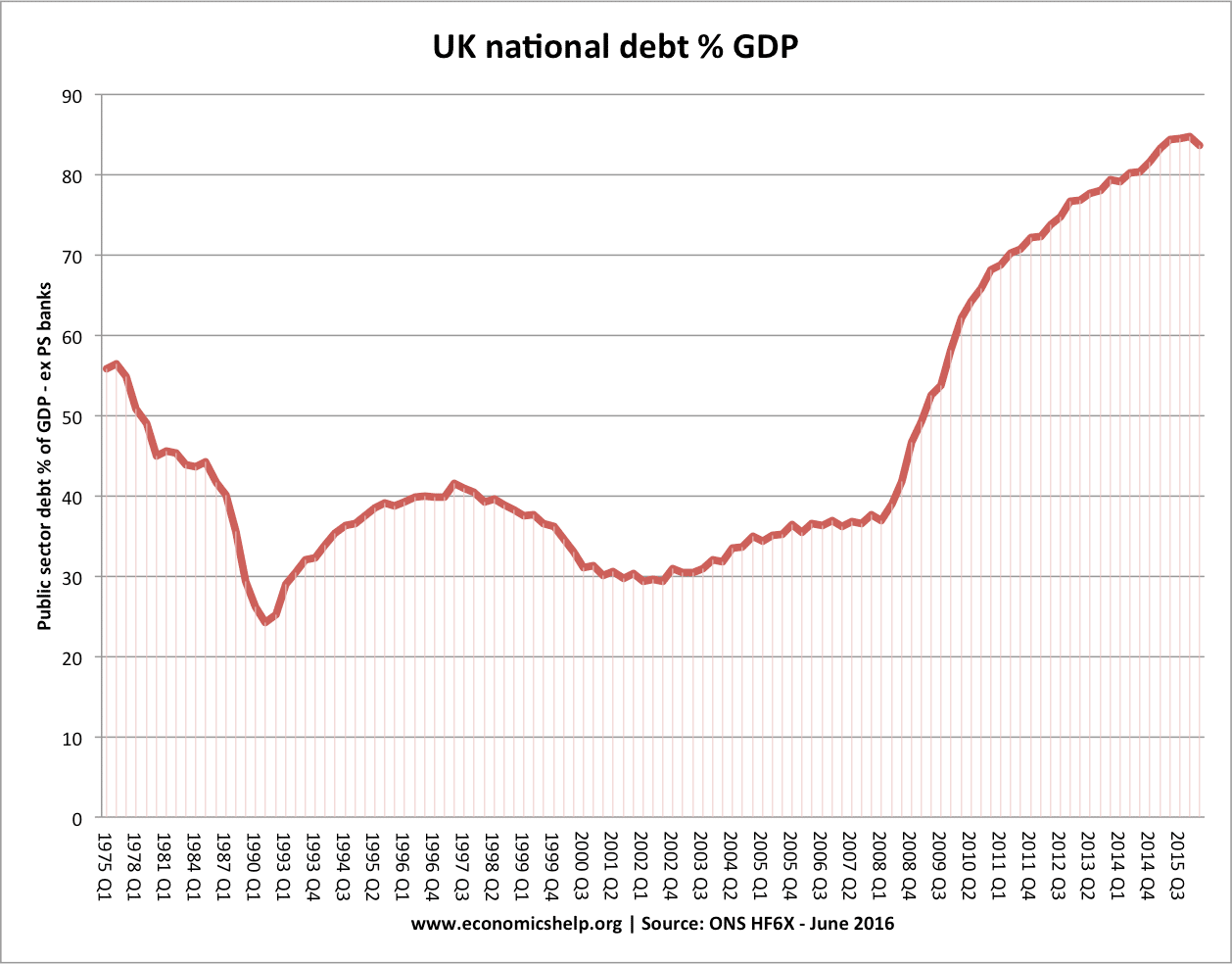

The US federal debt has again been on the move, as of mid-week up to a fresh record of $20.7 trillion. But, really, without some sort of reference point, what does that mean?

Typically, the metrics of total debt or federal debt divided by GDP (Gross Domestic Product, or the total value of goods produced and services provided in the US annually) are used (chart below). Still, that’s a bit ethereal to most folks.

So, I thought I’d make this simpler. The chart below shows federal debt (red line) versus total full-time employees (blue line) since 1970. Clearly, debt has surged since 2000 and particularly since 2008 versus decelerating net full-time jobs growth. The number of full-time employees is economically critical as, generally speaking, only these jobs offer the means to be a home buyer or build savings and wealth in a consumer-driven economy. Part-time employment generally offers only subsistence level earnings.

But if we look at the change over those periods highlighted in the chart above, we get a clear picture (chart below). Full-time jobs are being added at a rapidly declining rate while federal debt is surging in the absence of the growth of full-time employees.

The fiscal gap is a measure of a government’s total indebtedness proposed by economists Laurence Kotlikoff and Alan Auerbach, who define it as the difference between the present value of all of government’s projected financial obligations, including future expenditures, including servicing outstanding official federal debt, and the present value of all projected future tax and other receipts, including income accruing from the government’s current ownership of financial assets.[1] According to Kotlikoff and Auerbach, the “fiscal gap” accounting method can be used to calculate the percentage of necessary tax increases or spending reductions needed to close the fiscal gap in the long-run.

Generational accounting, an accounting method closely related to the fiscal gap, has been proposed by the same authors as a measure of the future burden of closing the fiscal gap. The “generational accounting” assumes that current taxpayers are neither asked to pay more in taxes nor receive less in transfer payments than current policy suggests and that successive younger generations’ lifetime tax payments net of transfer payments received rise in proportion to their labor earnings.

According to Kotlikoff and Auerbach, “fiscal gap accounting” and “generational accounting” reports have been done for roughly 40 developed and developing countries either by their treasury departments, finance ministries, or central banks, or by the IMF, the World Bank, or other international agencies, or by academics and think tanks.

Size of the U.S. fiscal gap

Fiscal gap accounting is not new to the U.S. government.[citation needed] The Social Security Trustees and Medicare Trustees have been presenting such calculations for their own systems for years in their annual reports.[citation needed] And generational accounting has been included in the President’s Budget on three occasions.[citation needed]

Based on calculations using the 2012 Alternative Fiscal Scenario long-term projections by the Congressional Budget Office, some estimate the U.S. fiscal gap stands to be $222 trillion – more than 13 times larger than the reported U.S. National Debt.[citation needed] According to the same estimates, the gap grew $11 trillion from 2011 to 2012.[citation needed] Eliminating the entire U.S. fiscal gap through revenue alone would require a permanent 64% increase in all federal taxes.[citation needed] Alternatively, closing the gap through spending reductions alone would require a permanent 40% cut in all federal purchases and transfer payments.[2]

Criticism of fiscal gap accounting

The proposed “fiscal gap” accounting method has been criticized as fundamentally flawed by economists Dean Baker,[3]Bradford DeLong,[4] and Paul Krugman.[5] Their critiques, referenced above, center on the fact that fiscal gap accounting calculates the growth future debt in current account terms, without taking into account the fact that future GDP will also grow proportionately, with the result that future debt will fall on generations with substantially larger incomes to cover the debt, obviating the seeming fiscal impossibility of covering the gap.

Kotlikoff’s thesis examined, in a life-cycle simulation model, the impact of intergenerational redistribution on the long-run position of the economy. He also studied whether the rich spend a larger or smaller share of their lifetime resources than do the poor. And he provided a new empirical approach to understanding the impact of Social Security on saving. At UCLA, Kotlikoff wrote a paper with Avia Spivak on intra-family risk-sharing entitled “The Family as an Incomplete Annuities Market.”[2]

He also wrote a widely cited paper with Lawrence Summers questioning the importance of saving for retirement in determining total U.S. wealth accumulation.[3] The publication suggested that most of U.S. wealth accumulation was not attributed to life-cycle saving, but rather to private intergenerational transfers (whether intended or unintended).[3] The article was the subject of a lively debate between Kotlikoff and Franco Modigliani, who won the Nobel Prize in part for his work on the life-cycle model.[4]

Kotlikoff, together with Alan Auerbach and Jagadeesh Gokhale, pioneered Generational Accounting, which measures the fiscal burdens facing today’s and tomorrow’s children.[5] Kotlikoff’s work on the relativity of fiscal language claims to show that conventional fiscal measures, including the government’s deficit, are not well defined from the perspective of economic theory.[citation needed]

According to Kotlikoff, their measurement reflects economically arbitrary fiscal labeling conventions.[citation needed] He argues that an “Economics labeling problem,” as he calls it, has led to gross misreadings of the fiscal positions of different countries, starting with the United States, which has a relatively small debt-to-GDP ratio, but, he argues, is in worse fiscal shape than any other developed country.[citation needed] In 1991, Kotlikoff, together with Alan Auerbach and Jagadeesh Gokhale, produced the first set of generational accounts for the United States.[citation needed]

Their study claimed to find a major fiscal gap separating future government spending commitments and its means of paying for those commitments, portending dramatic increases in the lifetime net tax burdens facing young and future generations.[citation needed] The generational accounting and fiscal gap accounting developed by Auerbach, Gokhale, and Kotlikoff is a means of assessing the sustainability of fiscal policy and how different countries intend to treat their next generations.[citation needed] Recent generational accounting by the IMF and fiscal gap accounting by Kotlikoff claim to confirm the truly severe long-run fiscal problems facing the U.S.[citation needed]

In the late 1970s, Kotlikoff, together with Berkeley economist, Alan J. Auerbach, developed the first large-scale computable general equilibrium life-cycle model that can track the behavior, over time, of economies comprising large numbers of overlapping generations.[6] The model and its offspring have been used extensively to study future fiscal and demographic transitions in the U.S. and abroad.[citation needed] Demographically realistic overlapping generations models, in which agents can live for up to, say, 100 years, are very complicated mathematical structures.[citation needed]

Agents who are young would, if they were rational and precognitive, consider all future interest rates and wage rates in deciding how much to save and work in the current as well as in their remaining future years.[citation needed] This path of interest rates and wage rates will, in turn, depend on the course of the economy’s relative supplies of capital and labor, since these relative supplies determine whether capital or labor is relatively scarce in any given future year and, therefore, what these factors of production will get paid in the competitive market.[citation needed]

The paths of capital and labor will be determined by the aggregation of the saving and labor supply decisions of the individual agents alive through time.[citation needed] Thus a young person’s decision about consuming and working today depends, in part, on what he believes will be the interest and wage rates when he’s middle age and old, for example, age 90.[citation needed] But the value of these factor prices when he’s age 90 depend on how much capital and labor will be around in that year.[citation needed]

This depends, in part, on the saving and labor supply of unborn generations who will be saving and working when he reaches old age.[citation needed] In short, the economic decisions of one generation are interlinked with those of others because of general equilibrium considerations in which each year’s collective supplies of capital and labor must equal that year’s aggregate demands for these inputs.[citation needed] And the path of interest and wage rates must be such as to clear (equate supplies to their respective demands) these factor markets at each point in time.[citation needed]

Under standard assumptions about the nature of technology and in the simplest framework (which can be extended to more than two inputs), this problem devolves into a 200-plus order non-linear difference equation in the ratio of capital to labor.[citation needed] This ratio summaries both the relative supplies of and demands for the two factors. In equilibrium, the ratio of factor inputs supplied each year must equal the ratio of factor inputs demanded.[citation needed]

Since the path of the capital-labor ratio determines the path of the interest and wage rate, which determine both the annual supply of and demand for the two factors of production, the problem boils down to finding the precise path of the capital-labor ratio that will draw forth from extant households each year aggregate supplies of capital and labor that exactly match each year’s respective aggregate demands for capital and labor by firms.[citation needed]

There are no mathematical techniques for calculating the exact solution of high order non-linear difference equations.[citation needed] (The Scarf Algorithm cannot be used in this context because the number of markets is infinite; i.e., there is no assumed end of the world.) Auerbach and Kotlikoff devised an iterative solution method that entails guessing how the economy’s ratio of capital to labor will evolve and then updating the guesses based on deviations of annual capital and labor supplies from their respective annual demands and continuing in this manner until the economy’s capital-labor transition path converges to a fixed-point path (more precisely, until the guessed ratio of the annual demands for capital relative to labor equal the annual supplies of capital relative to labor).[citation needed]

Prior to the development of the Auerbach-Kotlikoff model, economists had no means of assessing how a realistic life-cycle economy would evolve, including the timing of its responses to a wide range of fiscal and demographic changes.[citation needed] For example, economists had no means of saying how much capital would be available to the economy in each future year were the government to increase its consumption on a permanent basis and finance that higher level of consumption by raising income tax rates.[citation needed]

One of the latest incarnations of the Auerbach-Kotlikoff model – a paper by Hans Fehr, Sabine Jokisch, and Laurence Kotlikoff entitled “Dynamic Globalization and Its Potentially Alarming Prospects for Low-Wage Workers,” includes five regions (the U.S., Europe, Japan, China, and India), six goods, region-specific fiscal policy and demographics, and the endogenous determination of the pattern of specialization.[citation needed]

The general relativity of fiscal language

In 1984, Kotlikoff wrote a fundamental paper entitled “Deficit Delusion”, which appeared in The Public Interest. This was the first of a series of papers and books (see, e.g., Generational Accounting and Generational Policy) by Kotlikoff, including work with co-authors, showing, via examples, that in economic models featuring rational agents, “the” deficit is a figment of language, not economics. I.e., the deficit is not economically well defined. Instead, what governments measure as “the” deficit is entirely a result of the language they use to label government receipts and payments.[citation needed]

If the government calls a receipt a “tax,” this lowers the reported deficit. If, instead, it calls the receipt “borrowing,” it raises the reported deficit. Thus, if you give the government, say, $1,000 this year, it can say it is taxing you $1,000 this year. Alternatively, it can say it is borrowing $1,000 from you this year and will be taxing you in, say, five years the $1,000 plus accrued interest and using this future tax to pay you the principal plus interest due on the current borrowing. With one set of words the deficit is $1,000 larger this year than with the other set of words.[citation needed]

If it so chose, the government could say it was taxing you $1,000 this year and also, this year, borrowing $1 trillion from you for, say, five years, making a transfer payment to you this year of $1 trillion, and taxing you in five years an amount equal to principal plus interest on the $1 trillion and using it to pay principal plus interest on the $1 trillion it is now borrowing. With this alternative choice of words, the reported deficit is $1 trillion larger than with the first set of words. But in all three examples, you hand over $1,000 this year and receive and pay zero on net in the future.[original research?]

Einstein taught us that neither time, nor distance are well-defined physical concepts. Instead, their measurement is relative to our frame of reference – how fast we were traveling in the universe and in what direction. Our physical frame of reference can be viewed as our language or labeling convention. Einstein showed that neither time nor distance were well-defined concepts, but could be measured in an infinite number of ways. The same is true of the deficit. Just like absolute time and distance are not well defined, the deficit and related conventional fiscal measures has no economic meaning.[citation needed][original research?]

Kotlikoff, along with Harvard’s Jerry Green, offered a general proof of the proposition that deficits and a number of other conventional fiscal measures are, economically speaking, content-free, concluding that the deficit is simply an arbitrary figment of language in all economic models involving rational agents.[7]

Such models can feature all manner of individual and aggregate uncertainty, incomplete markets, distortionary fiscal policy, asymmetric information, borrowing constraints, time-inconsistent government policy, and a host of other problems, yet “the” deficit will still bear no theoretical connection to real policy-induced economic outcomes.[citation needed][original research?] The reason, again, is that there is no single deficit, but rather an infinity of deficit or surplus policy paths that can be announced (by the government or any private agent) simply by choosing the “right” fiscal labels.[citation needed][original research?]

Frames of reference

According to Kotlikoff, using the deficit as a guide to fiscal policy is like driving in Los Angeles with a map of New York City.[citation needed] For unlike in our physical world in which we are all using the same language (have the same frame of reference), in the world of economics, we are each free to adopt our own frame of reference – our own labeling convention. Thus, if Joe wants to claim that the U.S. federal government ran enormous surpluses for the last 50 years, he can simply choose appropriate words to label historic receipts and payments to produce that time series.[citation needed]

If Sally wishes to claim the opposite, there are words she can find to justify her view of the past stance of fiscal policy. And if Sam wishes to claim that that economy has experienced fluctuations from deficits to surpluses of arbitrary magnitude from year to year, he can do so. Language is extremely flexible. And there is nothing in economic theory that pins down how we discuss economic theory.[citation needed]

Kotlikoff and Green claim that fiscal variables in all mathematical economic models involving rational agents can be labeled freely and tell us nothing about the models themselves (no more than does choosing to discuss the models in French or English), and this means that the multitudinous econometric studies relating well-defined economic variables, such as interest rates or aggregate personal consumption, to “the” deficit are, economically speaking, content free.[citation needed]

According to Kotlikoff, the deficit is not the only variable that is not well defined.[citation needed] An economy’s aggregate tax revenue, its aggregate transfer payments, its disposable income, its personal and private saving rates, and its level of private wealth – all are non-economic concepts that have, from the perspective of economic theories with rational agents, no more purchase on economic reality than does the emperor’s clothes in Hans Christian Andersen’s famous children’s story.[citation needed]

Kotlikoff chose the title of his paper with Green not to suggest in the slightest any comparison of intellect with Einstein,[original research?] but rather because of what seemed to him to be a strikingly similar message about confusing linguistics for substance.[citation needed] An example here is the definition of a capitalistic economy as one in which capital is primarily owed by the private sector. Kotlikoff claims that an economy which is described as having predominately privately owned wealth can just as well be described as one in which wealth is predominantly or, for that matter, entirely state-owned.[citation needed] Hence, “deficit delusion” implies that economic theory offers no precise measure/definition of capitalism, socialism, or communism.[citation needed]

Intergenerational altruism

Kotlikoff has done pioneering[peacock term] work testing intergenerational altruism[citation needed] – the proposition that current generations care about their descendants enough to ensure that government redistribution from their descendants to themselves will be offset by private redistribution back to the descendants either in the form of bequests or intervivos gifts. This proposition dates to David Ricardo, who raised it as a theoretical, but empirically irrelevant proposition.[citation needed]

In 1974, Robert Barro revived “Ricardian Equivalence” by showing in a simple, elegant framework that each generation’s caring about its children leads current generations to be altruistically linked to all their descendants. Hence, a government policy of transferring resources to current older generations at a cost to generations born, say, in 100 years would induce the current elderly to simply increase their gifts and bequests to their children who would pass the resources onward until it reached those born in 100 years.[citation needed]

This inter-linkage of current and future generations devolves into a mathematical model which is isomorphic to one in which all agents are infinitely lived (i.e., they act as if they live for ever in so far as their progeny are front and center in their preferences). The infinitely-lived model was originally posited by Frank Ramsey in the 1920s. It’s aggregation properties make it very convenient for teaching macro economics because one does not have to deal with the messiness of upwards of 100 overlapping generations acting independently, but also interdependently. Consequently, it has become a mainstay in graduate macroeconomics training and underlies the work by Economics Nobel Laureate Ed Prescott and other economists on Real Business Cyclemodels.[citation needed]

Kotlikoff’s singly and jointly authored work in the 1980s and 1990 called this model into question on both theoretical and empirical grounds. In a paper entitled “Altruistic Linkages within the Extended Family: A Note (1983),” which appears in Kotlikoff’s 1989 MIT Press book What Determines Savings? Kotlikoff showed that when agents take each other’s transfers as given, marriage generates intergenerational linkages between unrelated individuals.[citation needed]

I.e., if you, Steve, are altruistic toward your daughter, Sue, and your daughter marries John, who is altruistically linked to his father Ed, who has a daughter Sara who is altruistic toward her husband David, who cares about his sister Ida, who’s cares about her father-in-law Frank, you Steve are altrusitically linked to Frank. Furthermore, if Frank loses a dollar and you gain a dollar, Barro’s model implies that you Steve will take your new found dollar and hand it to Frank. Kyle Bagwell and Douglas Bernheim independently reached Kotlikoff’s conclusion, namely that the Barro model had patently absurd implications.[citation needed]

Together with Assaf Razin and Robert Rosenthal, Kotlikoff showed in [4] that dropping the unrealistic assumption that transfers are taken as given and permitting individuals to refuse transfers (e.g., refusing your mother’s offer of an extra helping of cabbage) invalidates Barro’s proposition of Ricardian Equivalence. I.e., they showed that Barro’s model was a combination of a plausible set of preferences (altruism toward one’s children) and an implausible assumption about the game being played by donors and donees. In a series of empirical papers with Stanford economist Michael Boskin, University of Pennsylvania economist Andrew Abel, Yale economist Joseph Altonji, and Tokyo University economist Fumio Hayashi, Kotlikoff and his co-authors showed that there was little, if any, empirical support for Barro’s very special model of intergenerational altruism.[citation needed]

Generational redistribution

In life-cycle models without operative intergenerational altruism, the young are the big savers because of every dollar they receive, they save a larger percentage than do the elderly for the simple reason that the elderly are closer to the ends of their lives and want to use it before they lose it. The unborn are, of course, the biggest savers because giving them an extra dollar (that they will be able to collect with interest when they arrive) leads them to consume nothing more in the present because they aren’t yet alive.[citation needed]

So taking from the young and unborn and giving to the elderly should lead to a decline in national saving. In a 1996 paper with Jagadeesh Gokhale and John Sablehaus, Kotlikoff showed that the ongoing massive redistribution from young and future savers to old savers was responsible for the postwar decline in U.S. saving.[8]

Notwithstanding his many studies overturning Ricardian Equivalence, on both theoretical and empirical grounds, Kotlikoff has a paper showing why intergenerational transfers may have no impact on the economy in a world of purely selfish life-cycle agents. The argument presented is simple. Once younger generations have been maximally exploited by older generations (who are assumed to have the ability to redistribute from the young to themselves), older generations can no longer extract resources for free, meaning they can no longer leave higher fiscal burdens for future generations without handing over a quid pro quo. At such an extreme, intergenerational transfers, per se, are no longer feasible because the young will refuse to accept them.[citation needed]

Kotlikoff has been a supporter of the FairTax proposal as a replacement for the federal tax code, contributing to research of plan’s effects and the required rate for revenue neutrality.[10] In 2010, Kotlikoff offered his own tax proposal, titled the Purple Tax (a blend of red and blue), a consumption levy that he says cleans up some problems with the FairTax.[11][12]

His plan calls for a 15% final (17.5% nominal) sales tax. The FICA tax ceiling is gone and the 7.65% of the employees contribution is applied on everything after $40,000 but the employer pays 7.65% on the employees entire salary.[13]

Finance

Kotlikoff’s proposed reform of the financial system,[14][15][16] discussed in Jimmy Stewart Is Dead, called Limited Purpose Banking, transforms all financial companies with limited liability, including incorporated banks, insurance companies, financial exchanges, and hedge funds, into pass-through mutual funds, which do not borrow to invest in risky assets, but, instead, allows the public to directly choose what risks it wishes to bear by purchasing more or less risky mutual funds.[17] According to Kotlikoff, Limited Purpose Banking keeps banks, insurance companies, hedge funds and other financial corporations from borrowing short and lending long, which leaves the public to pick up the pieces when things go south.[17] Instead, Kotlikoff argues Limited Purpose Banking forces financial intermediaries to limit their activities to their sole legitimate purpose—financial inter-mediation.[17] It would substitute the vast array of extant federal and state financial regulatory bodies with a single financial regulator called the Federal Financial Authority (FFA), which would have a narrow purpose namely to verify, disclosure, and oversee the independent rating and custody off all securities purchased and sold by mutual funds.[17]

Healthcare

In his 2007 book, The Healthcare Fix, Kotlikoff proposed a major reform of the U.S. healthcare system, subsequently dubbed “The Purple Health Plan”,[18] that would do away with Medicare, Medicaid, employer-based healthcare, and health exchanges established under the Affordable Care Act.[19] In their place, every American would receive a voucher for a basic health insurance policy, whose coverages would be established by a panel of doctors such that the total cost of all vouchers remained within a fixed share, e.g., 10 percent, of GDP.[18][19] The voucher would be provided by the government at no cost and its amount would be individually risk-adjusted, i.e., sicker people would receive larger vouchers.[18][19] No health insurance company providing the basic insurance plan could turn anyone away and those who could afford supplemental health insurance plans would be free to purchase them.[18][19]

According to Kotlikoff, the plan provides universal basic health insurance, retains private provision of healthcare, limits government healthcare spending to a fixed share of GDP, and avoids adverse selection.[18][19] Kotlikoff has denounced critics of the plan such as economist Paul Krugman and President Obama for demagoguery over word voucher—arguing that the current health care law relies on vouchers.[20] He argues that the current Medicare program is unsustainable and that we have no choice but to embrace a plan with vouchers.[21] In order to highlight his Purple Plans, Kotlikoff ran for the nomination of the Americans Elect platform in its short-lived effort to field a third party candidate in the 2012 Presidential election.

Political parties

Kotlikoff fervently dislikes both political parties and has called for a third party.[22] In January 2012, Kotlikoff announced his plans to run as a third party candidate for President of the United States in 2012. Kotlikoff said he would seek the presidential nomination of the non-partisan advocacy group Americans Elect.[1][23][24] He announced in May that he would also seek the nomination of the Reform Party of the United States,[25] but ended the bid after the Americans Elect board decided to not field a 2012 presidential ticket.[26]

Other ventures

Kotlikoff is the President of Economic Security Planning, Inc., a company that markets ESPlanner, an economics-based personal financial planning software program,[27] a simplified version of which is available on-line for free use by the public,[28] and “Maximize My Social Security”, a software program that helps Americans decide which Social Security benefits to take and when, to get the highest lifetime benefits.[29]

Books

The Economic Consequences of the Vickers Commission, Civitas, 2012.

The Clash of Generations, (with Scott Burns), MIT Press, 2012.

Jimmy Stewart is Dead – Ending the World’s Ongoing Financial Plague with Limited Purpose Banking. John Wiley and Sons, 2010.

Spend ‘Til the End – The Revolutionary Guide to Raising Your Living Standard, Today and When You Retire. Simon & Schuster, (with Scott Burns), 2008.

The Healthcare Fix – Universal Insurance for All Americans, MIT Press, 2007.

The Coming Generational Storm, (with Scott Burns), MIT Press, 2004.

Generational Policy, The 2002 Caroli Lectures, MIT Press, 2003.

Essays on Saving, Bequests, Altruism, and Life-Cycle Planning, MIT Press, 2001.

Generational Accounting Around the World, co-edited with Alan Auerbach and Willi Leibfritz, NBER volume, University of Chicago Press, 1999.

Macroeconomics: An Integrated Approach Second Edition, (with Alan Auerbach), MIT Press, 1998.

Macroeconomics: An Integrated Approach (with Alan Auerbach), Southwestern Publishing Co., 1994.

Generational Accounting, The Free Press, 1992.

What Determines Savings, MIT Press, 1989.

The Wage Carrot and the Pension Stick: Retirement Benefits and Labor Force Participation(with David Wise), The W. E. Upjohn Institute for Employment Research, 1989.

Dynamic Fiscal Policy (with Alan Auerbach), Cambridge University Press, 1987.

Pensions in the American Economy (with Daniel Smith), University of Chicago Press, 1983.

Get What’s Yours: The Secrets to Maxing Out Your Social Security (with Philip Moeller and Paul Solman), Simon and Schuster, 2015.[30]

Laurence J. Kotlikoff and Scott Burns (2004). The Coming Generational Storm: What You Need to Know about America’s Economic Future’. MIT Press. ISBN0-262-11286-8. Descriptionand chapter-preview links, p. vii.

Laurence J. Kotlikoff and Scott Burns, 2008. Spend ’til the End: The Revolutionary Guide to Raising Your Living Standard – Today and When You Retire’, Simon & Schuster. Descriptionand Preview link to chapter links, via right-arrow at top to pp. 11–12.

^Gokhale, Jagadeesh; Kotlikoff, Laurence J.; Sabelhaus, John (May 1996). “Understanding the Postwar Decline in U.S. Saving: A Cohort Analysis”. NBER Working Paper No. 5571. doi:10.3386/w5571.

^ Jump up to:abcdKotlikoff, Laurence (April 5, 2011). Jimmy Stewart Is Dead: Ending the World’s Ongoing Financial Plague with Limited Purpose Banking. Wiley. ISBN978-1118011331.

The national debt exceeded $21 trillion for the first time on Thursday, a little more than six months after it hit first $20 trillion on Sept. 8.

The national debt was $21.031 trillion on Thursday. The government releases total debt figures each business day, but it lags by one day.

Federal borrowing has been on the rise again since February, when Congress passed legislation to suspend the debt ceiling. That move allowed the government to borrow as much as it needs to fund the activities approved by Congress.

Under the law passed in February, the government will not face any borrowing limit until March 1, 2019. At its current pace, the government is on track to add at least $1 trillion to the national debt by then.

For example, the debt grew by more than half a trillion dollars in the six weeks since the debt ceiling was lifted on Feb. 9.

A large part of the national debt reflects the federal budget deficit, or the amount of spending above the revenues collected by the government. But the debt is rising faster than the amount of the budget deficit, as it also reflects things like federal lending for student loans and mortgage programs.

Peter G. Peterson Foundation President Michael Peterson said the milemarker is just the beginning, as Congress has just agreed to spend even more.

“Our national debt reached a staggering $21 trillion today, having grown by $1 trillion in just the past six months,” he said. “Worse yet, this unfortunate milestone has only just begun to include the effects of the recent fiscally irresponsible tax and spending legislation, which added more debt on top of an already unsustainable trajectory.”

World’s Greatest Memory and Trump’s La la Land | David Stockman’s Warning

Published on Apr 29, 2017

You can also check out the following:

David Stockman’s Warning

Jim Sinclair

James Turk

Web bot

Silver News

Gold

Bix Weir

RoadToRoota

Road To Roota

Kyle Bass

Realist News

Greg Mannarino

Rob Kirby

Reluctant Preppers

The Next Newss

Info Wars

Maneco64

Mike Maloney

Gold Silver

Eric Sprott

Jim Rickards

David Morgan

Peter Schiff

Max Keiser

Robert Kiyosaki

SilverDoctors

Finance and Liberty

Nomi Prins

Jim Willie

Clif High

Martin Armstrong

Ron Paul

Pastor Williams

Bill Holter

Bo Polny

Jim Sinclair

James Turk

Clif High

Stockman on Trump’s Tax Plan: ‘Borrowing Money Is Not the Way to Prosperity’

David Stockman: National debt is ticking time bomb

David Stockman: Trump doesn’t know anything about tax policy

David Stockman: We’re wasting money on defense

David Stockman on Trump’s wall: I think it’s a stupid idea

David Stockman: Economy is on the edge of ruin

David Stockman: We’ll have a fiscal bloodbath, not fiscal stimulus

David Stockman Trumps Efforts To Drain The Swamp

David Stockman – Trump Will Create A Debt Crisis Like Never Before – 28 Feb 17 | Gazunda

David Stockman – Global Deflation As A Result Of Massive Over-investment – 9 Feb 16 | Gazunda

David Stockman Speaks on Shakeup Expected At The White House. #TheWhiteHouse

David Stockman: We are at peak debt headed for a recession

David Stockman on Trump’s infrastructure spending

RTD News: “A 20 Trillion Ticking Time Bomb…” – David Stockman

David Stockman: We have a massive bubble in the market

David Stockman -Trump Can’t Stop Market Crash Predicts Reagan’s Budget Director

Stockman: U.S. election is Brexit on steroids

[74] David Stockman | One Big Fat Ugly Bubble

David Stockman: Lester Holt was in the tank for Hillary Clinton

Stockman: Janet Yellen is a clueless economist

David Stockman: What the Fed and the Feds Have Done to Us, and How to Reverse It

David Stockman: Why a Trump Presidency Is Very Possible

What Trump Should Do – With David Stockman

David Stockman Bubbles, Economic Collapse Coming 1

Robert Kiyosaki David Stockman discuss the biggest financial crisis in US history present,future

David Stockman: The US Is Fiscally, Morally, Intellectually Bankrupt

RTD News: “There Will Be No Rescue Out Of Washington This Time” – David Stockman

David Stockman – Conversations with Casey

How Crony Capitalism Corrupts the Free Market | David Stockman

The Forgotten Cause of Sound Money | David Stockman

Stockman: Market Will Not Be Pretty Under Trump

[Ed. Note: To see exactly what this former Reagan insider has to say about Trump and specifically what he believes must be done to drain the swamp, David Stockman is sending out a copy of his book Trumped! A Nation on the Brink of Ruin… And How to Bring It Back out to any American willing to listen. To learn how to get your free copy CLICK HERE.]

As bonds break a three day win streak and the U.S market hitting new record highs with a trifecta of records, CNBC was roaring about what to expect going forward. The Daily Reckoning contributor David Stockman joined Courtney Reagan to discuss what to expect going forward.

After the CNBC host positioned the critiques offered by David Stockman of the Trump administration she asked whether that would continue given the state of the market. Stockman did not mix words beginning the conversation with, “What’s going on today is complete insanity. The market is apparently pricing in a huge Trump stimulus package, when if you just look at the real world out there the only thing that is going to happen is a fiscal bloodbath and a White House train wreck like never before in U.S history.

How much more evidence do these so called traders need? Trump is lost in Twitter-land and he is out of control. He is turning out to be a complete jackass in the Oval Office. Co-President Bannon is off the deep end on terrorism, travel bans, Mexican walls, immigrant bashing and protectionism.”

David Stockman is a former Reagan Administration official who was the Office of Management and Budget Director. He also served as a two-term Congressman from the great state of Michigan. His latest book, Trumped! A Nation on the Brink of Ruin… And How to Bring It Back is out now. It offers his insight and exclusive analysis on exactly what the newly elected president must do in order to succeed in the White House. To get your own FREE copy, CLICK HERE to learn how.

“[They are] having nothing to do with the economic agenda and Trump has got an empty economic bench. He’s got no Secretary of the Treasury, no Office of Management and Budget, no Council of Economic Advisor Chairman. By this time, when I was there with the Reagan Administration, the plan was ready to go and he was going to Congress within a couple of days into February. We have a debt ceiling freight train coming down the road which will hit March 15 and then the cash will start running out and the system will be on edge. All of the continuing resolutions expire in April.”

“They are going to spend the year trying to repeal and replace Obamacare and it will be a fiasco. Nothing is going to happen this year. I don’t even think they can pass the budget resolution. There is going to be no tax action this year. If there is any bill next year it is going to be deficit neutral. Which means it is not going to add $15 to earnings like these crazy people expect.”

“Why would you be trading in this market, with this kind of chaos emerging everywhere at twenty six times trailing earnings? That’s where we are. It is completely crazy and it is only a question of how many more days or weeks that this kind of fantasy land can last.”

Courtney Reagan then pressed back asking, “At what point do you give in and admit that [Trump] is atypical but maybe he could get things done? I mean, look at all of the CEO’s that Trump has met with.” The former Reagan insider remarked that, “CEO’s come and go with every president. They came in with Reagan, they tell a president what they want to hear. These guys are just selling the song and dance about how many jobs they’re going to create in the next five years. They have no clue.”

“If we have a recession in the next five years, which surely we will, because recessions have not been outlawed and we haven’t had one for ten years. None of this stuff is going to happen. This is meaningless. What is meaningful is that Trump is out of control. This tweeting and getting off track on all of this terrorism stuff. This is a sign that there is going to be no governing coalition and that all of this fiscal stimulus expected by Wall Street is a complete fantasy. It can’t happen.”

Rickards’ Reaction: A Model For Predicting Financial Collapse

Jim Rickards’ reveals the only model you need to safe guard your wealth from the next financial crisis. In this 5-part exclusive framework a former Wall Street and intelligence community insider breaks down his analysis into a model to warm of impending financial collapse. The model is designed to offer the easiest and fastest way to apply hard facts, science and good sound analysis. Sign up for the Daily Reckoning e-letter today and receive your FREE report.

We will NOT share your email address

When CNBC then turned over the camera to a day trader who asked about the positive sentiment that exists within the market regarding Trump and his plan to deregulate Stockman stayed true to message. “Trump is just putting out press releases and the guise of Executive Orders. All of this stuff is going to get litigated, it goes through a rulemaking process, that takes years. So the relief on regulation will be important, but it way down the road and it won’t be that impactful.”

“The second thing, is we’re at 92 months in this expansion already. It is running out of gas. You can’t expect it to run forever. That is seemingly what is priced in by the market.”

“The third thing is, we have a giant debt and deficit problem. The debt ceiling is coming back into play it will be 20 trillion when it freezes in on March 15th. I’ll tell you this, people aren’t paying attention to the fact that Trump will never get a debt ceiling increase through the Congress without a government shutdown. When that happens it is, “bar the doors” because nobody is expecting it. We need to look at the facts, not the hopes.”

As the CNBC affirmed, it is not clear that the market is just going to drop tomorrow and history will repeat itself, Stockman repositioned. “The market it clearly factoring in a big Trump stimulus and I think anybody down there would admit if it doesn’t happen, if we get zero tax cuts, if we get a fiscal bloodbath in the Washington I am describing – the market is not going to stay where it is today at these absurd multiples of earnings.”

“This is all based on the idea that there is going to be a surge of economic growth and that profits are going to come back from about $89 a share by basis, where they were during the last twelve months, to a potential $110 or $130. My argument is there is not going to be any economic rebound. There is not going to be any profit surge. Therefore the market will be repricing dramatically downward once it is clear.”

Another CNBC analysis asked why – with the positive trends in jobless claims, manufacturing increasing, interest rates at near record lows – would the market not close out the year near record levels? “The market is assuming that profits are going to rebound. That we are not going to have any market dislocation and that nobody is going to be pushing back on Trump. It is hard to understand how people watching the day-to-day action down there could believe that.”

“Everybody is pushing back on Trump, he can’t even get his cabinet approved. He’s going to be bogged down in a Supreme Court fight, he’s going to be bogged down in a fight over a ridiculous travel ban. The idea that there is not going to be pushback is naive. What there is going to be is a train wreck. It is already clear that the people in the White House have no idea what they’re doing and it is only a matter of time before this honeymoon goodwill evaporates and the politicians get down to doing what they do best. Which is to undermine and obstruct anything that might be positive.”

When finally asked whether there is anything positive that would make him turn bullish in the near future he responded affirmably, “No, because Trump is inheriting thirty years of a disaster created by his predecessors. We have to take this $20 trillion of debt seriously. There is $10 trillion more built in under current policy, and that is without a dime of Trump tax cuts, infrastructure or stimulus. There is going to be a tremendous fiscal crisis in the years ahead which will prevent any of the kind of action that the “stimulus junkies” are looking for.

Stockman was born in Fort Hood, Texas, the son of Allen Stockman, a fruit farmer, and Carol (née Bartz).[2] He is of German descent, and his family’s surname was originally “Stockmann”.[3] He was raised in a conservative family, and his maternal grandfather, William Bartz, was a Republican county treasurer for 30 years.[4][5] Stockman was educated at public schools in Stevensville, Michigan. He graduated from Lakeshore High School in 1964[6] and received a B.A. in History from Michigan State University in 1968. He was a graduate student at Harvard University, 1968–1970 studying theology

Stockman was one of the most controversial OMB directors ever appointed, also known as the “Father of Reaganomics.” He resigned in August 1985. Committed to the doctrine of supply-side economics, he assisted in the passing of the “Reagan Budget” (the Gramm-Latta Budget), which Stockman hoped would curtail the “welfare state“. He thus gained a reputation as a tough negotiator with House Speaker Tip O’Neill‘s Democratic-controlled House of Representatives and Majority Leader Howard Baker‘s Republican-controlled Senate. During this period, Stockman became well known to the public during the contentious political wrangling concerning the role of the federal government in American society.

Stockman’s influence within the Reagan Administration was weakened after the Atlantic Monthly magazine published the infamous 18,246 word article, “The Education of David Stockman”,[7] in its December 1981 issue, based on lengthy interviews Stockman gave to reporter William Greider.

Stockman was quoted as referring to Reagan’s tax act in these terms: “I mean, Kemp-Roth [Reagan’s 1981 tax cut] was always a Trojan horse to bring down the top rate…. It’s kind of hard to sell ‘trickle down.’ So the supply-side formula was the only way to get a tax policy that was really ‘trickle down.’ Supply-side is ‘trickle-down’ theory.”[7] Of the budget process during his first year on the job, Stockman was quoted as saying, “None of us really understands what’s going on with all these numbers,” which was used as the subtitle of the article.[7]

After “being taken to the woodshed by the president” because of his candor with Greider, Stockman became concerned with the projected trend of increasingly large federal deficits and the rapidly expanding national debt. On 1 August 1985, he resigned from OMB and later wrote a memoir of his experience in the Reagan Administration titled The Triumph of Politics: Why the Reagan Revolution Failed in which he specifically criticized the failure of congressional Republicans to endorse a reduction of government spending to offset large tax decreases to avoid the creation of large deficits and an increasing national debt.

Fiscal legacy

President Jimmy Carter’s last fiscal year budget ended with a $79.0 billion budget deficit (and a national debt of $907,701,000,000 [8] as of September 30, 1980), ending during the period of David Stockman’s and Ronald Reagan’s first year in office, on October 1, 1981.[9] The gross federal national debt had just increased to $1.0 trillion during October 1981 ($998 billion on 30 September 1981, up from $907.7 billion during the last full fiscal year of the Carter administration[8]).

By 30 September 1985, four and a half years into the Reagan administration and shortly after Stockman’s resignation from the OMB during August 1985, the gross federal debt was $1.8 trillion.[8] Stockman’s OMB work within the administration during 1981 until August 1985 was dedicated to negotiating with the Senate and House about the next fiscal year’s budget, executed later during the autumn of 1985, which resulted in the national debt becoming $2.1 trillion at fiscal year end 30 September 1986.[8] Reaganomics had just begun.

In 1981, Stockman received the Samuel S. Beard Award for Greatest Public Service by an Individual 35 Years or Under, an award given out annually by Jefferson Awards.[10]

Business career

After leaving government, Stockman joined the Wall St. investment bank Salomon Brothers and later became a partner of the New York–based private equity company, the Blackstone Group.[11]:125–127 His record was mixed at Blackstone, with some very good investments, such as American Axle, but also failures, including Haynes International and Republic Technologies.[11]:144–147 During 1999, after Blackstone CEO Stephen A. Schwarzman curtailed Stockman’s role in managing the investments he had developed,[11]:146 Stockman resigned from Blackstone to start his own private equity fund company, Heartland Industrial Partners, L.P., based in Greenwich, Connecticut.[12]

On the strength of his investment record at Blackstone, Stockman and his partners raised $1.3 billion of equity from institutional and other investors. With Stockman’s guidance, Heartland used a contrarian investment strategy, buying controlling interests in companies operating in sectors of the U.S. economy that were attracting the least amount of new equity: auto parts and textiles. With the help of about $9 billion in Wall Street debt financing, Heartland completed more than 20 transactions in less than 2 years to create four portfolio companies: Springs Industries, Metaldyne, Collins & Aikman, and TriMas. Several major investments performed very poorly, however. Collins & Aikman filed for bankruptcy during 2005 and when Heartland sold Metaldyne to Asahi Tec Corp. during 2006, Heartland lost most of the $340 million of equity it had invested in the business.[13]

Collins & Aikman Corp.

During August 2003, Stockman became CEO of Collins & Aikman Corporation, a Detroit-based manufacturer of automotive interior components. He was ousted from that job days before Collins & Aikman filed for bankruptcy under Chapter 11 on May 17, 2005.

Criminal and civil charges

On March 26, 2007, federal prosecutors in Manhattan indicted Stockman in “a scheme… to defraud [Collins & Aikman]’s investors, banks and creditors by manipulating C&A’s reported revenues and earnings.” The United States Securities and Exchange Commission also brought civil charges against Stockman related to actions that he performed while CEO of Collins & Aikman.[14] Stockman suffered a personal financial loss, over $13 million, along with losses suffered by as many as 15,000 Collins & Aikman employees worldwide.

Stockman said in a statement posted on his law firm’s website that the company’s end was the consequence of an industry decline, not due to fraud.[15] On January 9, 2009, the US Attorney’s Office announced that it did not intend to prosecute Stockman for this case.[16]

Web site

In March 2014 Stockman launched a web based daily periodical, David Stockman’s Contra Corner featuring both his own articles and those from leading contrarian thinkers on geopolitics, economics, and finance.

This page is a candidate to be copied to Wikiquote using the Transwiki process. If the page can be expanded into an encyclopedic article, rather than a list of quotations, please do so and remove this message.

“[Social Security] has to be means-tested. And Medicare needs to be means-tested […] Let the Bush tax cuts expire. Let the capital gains go back to the same rate as ordinary income.”[20]

“The Republican Party has totally abdicated its job in our democracy, which is to act as the guardian of fiscal discipline and responsibility. They’re on an anti-tax jihad — one that benefits the prosperous classes.”[21]

“I invest in anything that Bernanke can’t destroy, including gold, canned beans, bottled water and flashlight batteries.”[22]

“Ninety-two percent of the wealth is owned by five percent of the people.” (Bloomberg TV 2013)

“[T]he Republican Party was hijacked by modern imperialists during the Reagan era. As a consequence, the conservative party cannot perform its natural function as watchdog of the public purse because it is constantly seeking legislative action to provision a vast war machine of invasion and occupation.” [23]

Bibliography

The Reagan Economic Plan, 1981

The Triumph of Politics: Why the Reagan Revolution Failed, Harper & Row, 1986, ISBN 9780060155605

The Great Deformation: The Corruption of Capitalism in America, PublicAffairs, 2013, ISBN 9781586489120

Trumped!: A Nation on the Brink of Ruin, and How to Bring it Back, 2016

^ Jump up to:ab“Collins & Aikman seeks to emerge from bankruptcy,” Bloomberg News article by Jeff Bennett, published in the newspaper The Advocate of Stamford and (identical version, perhaps with changes by the local editor in the common business section for both newspapers) in the Greenwich Time on September 5, 2006, page A7, The Advocate

Jump up^David Carey and Lou Whiteman, “PE firms find buyer for Metaldyne,” The Deal, Sept. 1, 2006.

What the Fed’s interest rate hike means for the economy

Stocks rally on Fed rate hike

Fed Hikes Rates, Signals More Coming

Is the Federal Reserve behind the curve?

What The Fed Rate Hike Means For Consumers

We Are Dangerously Close to a Recession

MARC FABER World Economy Grinding to a Halt. Don’t Trade With Leverage

Marc Faber : Volatility will pick up ‘massively’ , 30.1.2017

Marc Faber Warns : The Market is on the verge of a meaningful correction

Trump, China & World War 3 – Jim Rogers

The Whole System is Riddled With Corruption – James Dale Davidson Interview

Keiser Report: Rise of the Machines (E1043)

Keiser Report: Bloodletting Among Retailers (E1044)

David Stockman Interview Trump to Face Imploding Economy in 2017

David A. Stockman’s TEARS APART Trump’s Economic Plan

The Coming Big Freeze – Jim Rickards – The Daily Reckoning – Road to Ruin

James Rickards 2017 The Fed is Tapped Out & End Result is Ice Nine for Gold

AMTV Truth Exposed Prepare For The Imminent Global Economic Collapse 2017 Stock MARKET CRA

Fed rate hike: Central bank signals faster pace in 2017

Milton Friedman – The Federal Reserve Caused Great Depression

Milton Friedman on the Great Depression, Bank Runs & the Federal Reserve

Milton Friedman – Abolish The Fed

Milton Friedman: The Future of Freedom

Milton Friedman – Why Economists Disagree

Milton Friedman – The role of government in a free society

Milton Friedman Interview with Dallas Fed President Richard W. Fisher

Ep. 228: Inflation Finally Rears Its Head

What happens when the Fed raises rates

How Interest Rates Affect the Market

When Interest Rates Rise: Winners and Losers

ECONOMIC COLLAPSE: Trump to Declare Bankruptcy on U.S.

What’s all the Yellen About? Monetary Policy and the Federal Reserve: Crash Course Economics #10

The Federal Reserve Explained in 3 Minutes

Quantitative Easing Explained

The Collapse of The American Dream Explained in Animation

Who Controls the Money Controls the World

The Story of Your Enslavement

Financial Balance

“The Bernanke” explains Financial Repression

Financial Repression

Carmen Reinhart: Financial Repression Requires A Captive Audience | McAlvany Commentary

50 YEAR OLD CARTOON PREDICTS THE FUTURE !!! NWO !!!

Yellen Calms Fears Fed’s Policy Trigger Finger Is Getting Itchy

by Rich Miller, Christopher Condon , and Jeanna Smialek

March 15, 2017, 1:00 PM CDT March 15, 2017, 5:02 PM CDT

Policy makers still project three total rate hikes for 2017

FOMC sticks with ‘gradual’ plan for removing accommodation

Fed Raises Benchmark Lending Rate a Quarter Point

Federal Reserve Chair Janet Yellen sought to reassure investors that the central bank’s latest interest-rate increase wasn’t a paradigm shift to a trigger-happy policy driven by fears of faster inflation.

Speaking to reporters after the Fed’s quarter percentage-point move on Wednesday, Yellen said the central bank was willing to tolerate inflation temporarily overshootingits 2 percent goal and that it intended to keep its policy accommodative for “some time.”

“The simple message is the economy’s doing well. We have confidence in the robustness of the economy and its resilience to shocks,” she said.

As a result, the Fed is sticking with its policy of gradually raising interest rates, Yellen said. In their first forecasts in three months, Fed policy makers penciled in two more quarter-point rate increases this year and three in 2018, unchanged from their projections in December.

Today’s decision “does not represent a reassessment of the economic outlook or of the appropriate course for monetary policy,” the Fed chief said.

Speculation of a more aggressive Fed had mounted in recent days after a host of central bank officials, including Yellen herself, went out of their way to telegraph to financial markets that a rate hike was imminent. The expectations were further fueled by news of rising inflation.

Stocks Advance

Stocks rose and bond yields fell as investors viewed the statement from the Federal Open Market Committee and Yellen’s remarks afterward as a sign that the Fed isn’t in a hurry to remove monetary stimulus. The FOMC raised the target range for the federal funds rate to 0.75 percent to 1 percent, as expected, but Yellen’s lack of urgency to snuff out inflation was a surprise.

R.J. Gallo, a fixed-income investment manager at Federated Investors in Pittsburgh, said the chorus of Fed speakers before this meeting led investors to expect a move up in the number of projected rate hikes this year, and even upgrades by Fed officials in the levels of inflation and growth they anticipated.

None of that materialized.

“You didn’t get any of those things,” Gallo said, which explains why Treasury yields quickly dropped after the Fed released the FOMC statement and a new set of economic projections. “The expectation that Fed was getting more hawkish had to come out of the market.”

The U.S. economy has mostly met the central bank’s goals of full employment and stable prices, and may get further support if President Donald Trump delivers promised fiscal stimulus. Investor and business confidence has soared since Trump won the presidency in November, buoyed by his vows to cut taxes, lift infrastructure spending and ease regulations.

Still, the data don’t show an economy that’s heating up rapidly — a point Yellen herself made after the third rate hike since the 2007-2009 recession ended. In fact, the economy may have “more room to run,” she said.

Stronger business and consumer confidence hasn’t yet translated into increased investment and spending, said Yellen.

“It’s uncertain just how much sentiment actually impacts spending decisions, and I wouldn’t say at this point that I have seen hard evidence of any change in spending decisions,” said the Fed Chair. “Most of the business people that we’ve talked to also have a wait-and-see attitude.”

Retail sales in February grew at the slowest pace since August, a government report showed earlier Wednesday. The Atlanta Fed’s model for GDP predicts an expansion of 0.9 percent in the first quarter, less than a third the pace Trump is aiming for.

Fiscal Stimulus

Asked about the potential for a fiscal boost, Yellen made clear the Fed is still waiting for more concrete policy plans to emerge from the Trump administration before adapting monetary policy in reaction.

“There is great uncertainty about the timing, the size and the character of policy changes that may be put in place,” Yellen said. “I don’t think that’s a decision or set of decisions that we need to make until we know more about what policy changes will go into effect.”

Yellen disputed suggestions that the Fed was on a collision course with the Trump administration over its plans to foster faster economic growth through tax cuts and deregulation. “We would welcome stronger economic growth in the context of price stability,” she said.

She said she had met Trump briefly and had gotten together a couple of times with Treasury Secretary Steven Mnuchin to discuss the economy and financial regulation.

Further underscoring their lack of urgency, Fed officials repeated a commitment to maintain their balance-sheet reinvestment policy until rate increases were well under way. Yellen said officials had discussed the process of reducing the balance sheet gradually, but had made no decisions and would continue to debate the topic.

Policy makers forecast inflation will reach 1.9 percent in the fourth quarter this year, and 2 percent in both 2018 and 2019, according to quarterly median estimates released with the FOMC statement. The Fed’s preferred measure of inflation rose 1.9 percent in the 12 months through January, just shy of its target.

Yellen pointed out, though, that core inflation continues to run somewhat further below 2 percent. That rate, which strips out food and energy costs, stood at 1.7 percent in January. The Fed’s new forecast for the core rate at the end of this year edged up to 1.9 percent, from 1.8 percent in December.

“The committee will carefully monitor actual and expected inflation developments relative to its symmetric inflation goal,” the Fed said. Discussing the word symmetric in the statement, Yellen said during her press conference that the Fed was not shooting to push inflation over 2 percent but recognized that it could temporarily go above it. Two percent is a target, she reiterated, not a ceiling.

By Evan Tarver | Updated March 10, 2017 — 3:35 PM EST

SHARE

Changes in the federal funds rate will always affect the U.S. dollar. When the Federal Reserve increases the federal funds rate, it normally reduces inflationary pressure and works to appreciate the dollar.

Since June 2006, however, the Fed has maintained a federal funds rate of close to 0%. In the wake of the 2008 financial crisis, the federal funds rate fluctuated between 0-0.25%, and is now 0.75%.

The Fed used this monetary policy to help achieve maximum employment and stable prices. Now that the 2008 financial crisis has largely subsided, the Fed will look to increase interest rates to continue to achieve employment and to stabilize prices.

Inflation of the U.S. Dollar

The best way to achieve full employment and stable prices is to set the inflation rate of the dollar at 2%. In 2011, the Fed officially adopted a 2% annual increase in the price index for personal consumption expenditures as its target. When the economy is weak, inflation naturally falls; when the economy is strong, rising wages increase inflation. Keeping inflation at a growth rate of 2% helps the economy grow at a healthy rate.

Adjustments to the federal funds rate can also affect inflation in the United States. The Fed controls the economy by increasing interest rates when the economy is growing too fast. This encourages people to save more and spend less, reducing inflationary pressure. Conversely, when the economy is in a recession or growing too slowly, the Fed reduces interest rates to stimulate spending, which increases inflation.

During the 2008 financial crisis, the low federal funds rate should have increased inflation. Over this period, the federal funds rate was set near 0%, which encouraged spending and would normally increase inflation.

However, inflation is still well below the 2% target, which is contrary to the normal effects of low interest rates. The Fed cites one-off factors, such as falling oil prices and the strengthening dollar, as the reasons why inflation has remained low in a low interest environment.

The Fed believes that these factors will eventually fade and that inflation will increase above the target 2%. To prevent this eventual increase in inflation, hiking the federal funds rate reduces inflationary pressure and cause inflation of the dollar to remain around 2%.

Appreciation of the U.S. Dollar

Increases in the federal funds rate also result in a strengthening of the U.S. dollar. Other ways that the dollar can appreciate include increases in average wages and increases in overall consumption. However, although jobs are being created, wage rates are stagnant.

Without an increase in wage rates to go along with a strengthening job market, consumption won’t increase enough to sustain economic growth. Additionally, consumption remains subdued due to the fact that the labor force participation rate was close to its 35-year low in 2015. The Fed has kept interest rates low because a lower federal funds rate supports business expansions, which leads to more jobs and higher consumption. This has all worked to keep appreciation of the U.S. dollar low.

However, the U.S. is ahead of the other developed markets in terms of its economic recovery. Although the Fed raises rates cautiously, the U.S. could see higher interest rates before the other developed economies.

Overall, under normal economic conditions, increases in the federal funds rate reduce inflation and increase the appreciation of the U.S. dollar.

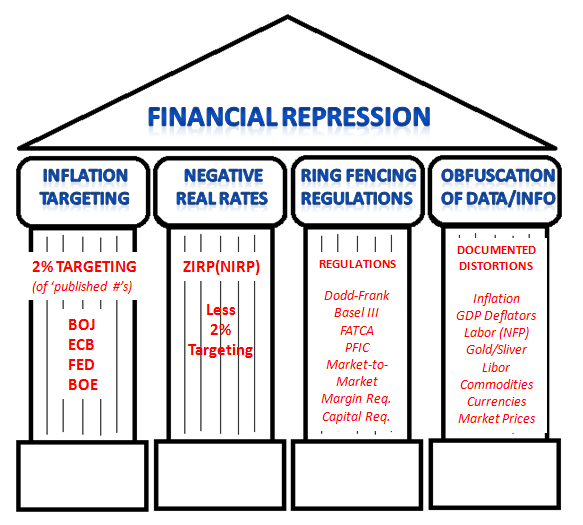

Not to be confused with economic repression, a type of political repression.

Financial repression refers to “policies that result in savers earning returns below the rate of inflation” in order to allow banks to “provide cheap loans to companies and governments, reducing the burden of repayments”.[1] It can be particularly effective at liquidating government debtdenominated in domestic currency.[2] It can also lead to a large expansions in debt “to levels evoking comparisons with the excesses that generated Japan’s lost decade and the Asian financial crisis” in 1997.[1]

Creation or maintenance of a captive domestic market for government debt, achieved by requiring banks to hold government debt via capital requirements, or by prohibiting or disincentivising alternatives.

Government restrictions on the transfer of assets abroad through the imposition of capital controls.

These measures allow governments to issue debt at lower interest rates. A low nominal interest rate can reduce debt servicing costs, while negative real interest rates erodes the real value of government debt.[5] Thus, financial repression is most successful in liquidating debts when accompanied by inflation and can be considered a form of taxation,[6] or alternatively a form of debasement.[7]

The size of the financial repression tax for 24 emerging markets from 1974 to 1987. Their results showed that financial repression exceeded 2% of GDP for seven countries, and greater than 3% for five countries. For five countries (India, Mexico, Pakistan, Sri Lanka, and Zimbabwe) it represented approximately 20% of tax revenue. In the case of Mexico financial repression was 6% of GDP, or 40% of tax revenue.[8]

Financial repression is categorized as “macroprudential regulation“—i.e., government efforts to “ensure the health of an entire financial system.[2]

Examples

After World War II

Financial repression “played an important role in reducing debt-to-GDP ratios after World War II” by keeping real interest rates for government debt below 1% for two-thirds of the time between 1945 and 1980, the United States was able to “inflate away” the large debt (122% of GDP) left over from the Great Depression and World War II.[2] In the UK, government debt declined from 216% of GDP in 1945 to 138% ten years later in 1955.[9]

China

China‘s economic growth has been attributed to financial repression thanks to “low returns on savings and the cheap loans that it makes possible”. This has allowed China to rely on savings-financed investments for economic growth. However, because low returns also dampens consumer spending, household expenditures account for “a smaller share of GDP in China than in any other major economy”.[1] However, as of December 2014, the People’s Bank of China “started to undo decades of financial repression” and the government now allows Chinese savers to collect up to a 3.3% return on one-year deposits. At China’s 1.6% inflation rate, this is a “high real-interest rate compared to other major economies”.[1]

After the 2008 economic recession

In a 2011 NBER working paper, Carmen Reinhart and Maria Belen Sbrancia speculate on a possible return by governments to this form of debt reduction in order to deal with high debt levels following the 2008 economic crisis.[5]

Critics[who?] argue that if this view was true, investors (i.e., capital-seeking parties) would be inclined to demand capital in large quantities and would be buying capital goods from this capital. This high demand for capital goods would certainly lead to inflation and thus the central banks would be forced to raise interest rates again. As a boom pepped by low interest rates fails to appear these days in industrialized countries, this is a sign that the low interest rates seem to be necessary to ensure an equilibrium on the capital market, thus to balance capital-supply—i.e., savers—on one side and capital-demand—i.e., investors and the government—on the other. This view argues that interest rates would be even lower if it were not for the high government debt ratio (i.e., capital demand from the government).

Free-market economists argue that financial repression crowds out private-sector investment, thus undermining growth. On the other hand, “postwar politicians clearly decided this was a price worth paying to cut debt and avoid outright default or draconian spending cuts. And the longer the gridlock over fiscal reform rumbles on, the greater the chance that ‘repression’ comes to be seen as the least of all evils”.[11]

Also, financial repression has been called a “stealth tax” that “rewards debtors and punishes savers—especially retirees” because their investments will no longer generate the expected return, which is income for retirees.[10][12] “One of the main goals of financial repression is to keep nominal interest rates lower than they would be in more competitive markets. Other things equal, this reduces the government’s interest expenses for a given stock of debt and contributes to deficit reduction. However, when financial repression produces negative real interest rates (nominal rates below the inflation rate), it reduces or liquidates existing debts and becomes the equivalent of a tax—a transfer from creditors (savers) to borrowers, including the government.”[2]

The interest rate that the borrowing bank pays to the lending bank to borrow the funds is negotiated between the two banks, and the weighted average of this rate across all such transactions is the federal funds effective rate.

The federal funds target rate is determined by a meeting of the members of the Federal Open Market Committee which normally occurs eight times a year about seven weeks apart. The committee may also hold additional meetings and implement target rate changes outside of its normal schedule.

Financial Institutions are obligated by law to maintain certain levels of reserves, either as reserves with the Fed or as vault cash. The level of these reserves is determined by the outstanding assets and liabilities of each depository institution, as well as by the Fed itself, but is typically 10%[4] of the total value of the bank’s demand accounts (depending on bank size). In the range of $9.3 million to $43.9 million, for transaction deposits (checking accounts, NOWs, and other deposits that can be used to make payments) the reserve requirement in 2007-2008 was 3 percent of the end-of-the-day daily average amount held over a two-week period. Transaction deposits over $43.9 million held at the same depository institution carried a 10 percent reserve requirement.

For example, assume a particular U.S. depository institution, in the normal course of business, issues a loan. This dispenses money and decreases the ratio of bank reserves to money loaned. If its reserve ratio drops below the legally required minimum, it must add to its reserves to remain compliant with Federal Reserve regulations. The bank can borrow the requisite funds from another bank that has a surplus in its account with the Fed. The interest rate that the borrowing bank pays to the lending bank to borrow the funds is negotiated between the two banks, and the weighted average of this rate across all such transactions is the federal funds effective rate.

The nominal rate is a target set by the governors of the Federal Reserve, which they enforce by open market operations and adjusting the interest paid on required and excess reserve balances. That nominal rate is almost always what is meant by the media referring to the Federal Reserve “changing interest rates.” The actual federal funds rate generally lies within a range of that target rate, as the Federal Reserve cannot set an exact value through open market operations.

Another way banks can borrow funds to keep up their required reserves is by taking a loan from the Federal Reserve itself at the discount window. These loans are subject to audit by the Fed, and the discount rate is usually higher than the federal funds rate. Confusion between these two kinds of loans often leads to confusion between the federal funds rate and the discount rate. Another difference is that while the Fed cannot set an exact federal funds rate, it does set the specific discount rate.

The federal funds rate target is decided by the governors at Federal Open Market Committee (FOMC) meetings. The FOMC members will either increase, decrease, or leave the rate unchanged depending on the meeting’s agenda and the economic conditions of the U.S. It is possible to infer the market expectations of the FOMC decisions at future meetings from the Chicago Board of Trade (CBOT) Fed Funds futures contracts, and these probabilities are widely reported in the financial media.

Applications

Interbank borrowing is essentially a way for banks to quickly raise money. For example, a bank may want to finance a major industrial effort but may not have the time to wait for deposits or interest (on loan payments) to come in. In such cases the bank will quickly raise this amount from other banks at an interest rate equal to or higher than the Federal funds rate.

Raising the federal funds rate will dissuade banks from taking out such inter-bank loans, which in turn will make cash that much harder to procure. Conversely, dropping the interest rates will encourage banks to borrow money and therefore invest more freely.[5] This interest rate is used as a regulatory tool to control how freely the U.S. economy operates.

By setting a higher discount rate the Federal Bank discourages banks from requisitioning funds from the Federal Bank, yet positions itself as a lender of last resort.

Comparison with LIBOR

Though the London Interbank Offered Rate (LIBOR) and the federal funds rate are concerned with the same action, i.e. interbank loans, they are distinct from one another, as follows:

The target federal funds rate is a target interest rate that is set by the FOMC for implementing U.S. monetary policies.

The (effective) federal funds rate is achieved through open market operations at the Domestic Trading Desk at the Federal Reserve Bank of New York which deals primarily in domestic securities (U.S. Treasury and federal agencies’ securities).[6]

LIBOR is based on a questionnaire where a selection of banks guess the rates at which they could borrow money from other banks.

LIBOR may or may not be used to derive business terms. It is not fixed beforehand and is not meant to have macroeconomic ramifications.[7]

Predictions by the market

Considering the wide impact a change in the federal funds rate can have on the value of the dollar and the amount of lending going to new economic activity, the Federal Reserve is closely watched by the market. The prices of Option contracts on fed funds futures (traded on the Chicago Board of Trade) can be used to infer the market’s expectations of future Fed policy changes. Based on CME Group 30-Day Fed Fund futures prices, which have long been used to express the market’s views on the likelihood of changes in U.S. monetary policy, the CME Group FedWatch tool allows market participants to view the probability of an upcoming Fed Rate hike. One set of such implied probabilities is published by the Cleveland Fed.

As of December 16, 2008, the most recent change the FOMC has made to the funds target rate is a 75 to 100 basis point cut from 1.0% to a range of zero to 0.25%. According to Jack A. Ablin, chief investment officer at Harris Private Bank, one reason for this unprecedented move of having a range, rather than a specific rate, was because a rate of 0% could have had problematic implications for money market funds, whose fees could then outpace yields.[8] This followed the 50 basis point cut on October 29, 2008, and the unusually large 75 basis point cut made during a special January 22, 2008 meeting, as well as a 50 basis point cut on January 30, 2008, a 75 basis point cut on March 18, 2008, and a 50 basis point cut on October 8, 2008.[9]

Explanation of federal funds rate decisions

When the Federal Open Market Committee wishes to reduce interest rates they will increase the supply of money by buying government securities. When additional supply is added and everything else remains constant, price normally falls. The price here is the interest rate (cost of money) and specifically refers to the Federal Funds Rate. Conversely, when the Committee wishes to increase the Fed Funds Rate, they will instruct the Desk Manager to sell government securities, thereby taking the money they earn on the proceeds of those sales out of circulation and reducing the money supply. When supply is taken away and everything else remains constant, price (or in this case interest rates) will normally rise.[10]