The Trump Way — Blood Oath — American People Want This Deal — The Chicago Way Not To Be Confused With Appeaser Obama’s Red Line Way — Videos

Trump responds to Iranian airstrike: Iran will never have a nuclear weapon

Special Report: Trump addresses Iran attack on U.S. bases in Iraq

Rep. Dan Crenshaw says Obama-era officials are obsessed with defending their appeasement of Iran

Tucker Carlson Tonight 1/8/20 | Fox News Today January 8, 2020

Sen. Ted Cruz on Sen. Mike Lee’s public frustration with intel briefing on Soleimani strike

Petraeus says U.S. had “lost the element of deterrence” before Soleimani strike

Iran strikes back at US with missile attack at bases in Iraq

Iran Strikes Back at U.S.With Missile Attack on Bases in Iraq | News 4 Now

Shields and Brooks on Iran general’s killing, 2020 Democrats’ fundraising

Trump says Iran will be hit ‘very fast’ if they strike American assets

The Chicago Way – The Untouchables (2/10) Movie CLIP

(1987) HD

A Clip From The Blind Side

The Blind Side

Donald Trump blames Barack Obama for giving Iran the cash to buy missiles flung at U.S. bases-as he offers to ’embrace peace’ and claims Tehran is ‘standing down’ but warns of ‘hypersonic weapons’ and ‘lethal and fast’ attacks

President said Iran can choose peace but warned of new weaponry that’s ready to strike

He blamed the Obama administration for unfreezing $150 billion and delivering $1.5 billion in cash to jump-start a nuclear nonproliferation deal that has since fallen apart

‘As long as I am president of the United States, Iran will never be be allowed have a nuclear weapon,’ he vowed, even before saying ‘Good morning’

‘Our missiles are big, powerful, accurate, lethal and fast,’ he said, sending a warning in nearly the same breath as an olive branch

‘Under construction are many hypersonic missiles,’ he warned, standing amid a tableau of stern-faced military leaders

Iran fired 22 ballistic missiles at two Iraqi bases housing American troops early Wednesday local time

Strikes are not thought to have killed any U.S. or Iraqi personnel, though extent of damage is being assessed

Ayatollah Khamenei said U.S. was given a ‘slap’ but strikes alone are ‘not enough’ and wants troops kicked out

There are still fears for U.S. troops after Iran-backed militias in Iraq threatened to carry out their own strikes

Donald Trump blamed Barack Obama on Wednesday for supplying Iran with the money to purchase a torrent of missiles fired at American military positions Tuesday night.

‘The missiles fired last night at us and our allies were paid for with the funds made available by the last administration,’ he said, citing $150 billion in frozen assets that the previous president released and $1.5 billion flown by the U.S. to Tehran.

He began his speech to the world on Wednesday with a familiar ultimatum, even before saying ‘Good morning.’

‘As long as I am president of the United States, Iran will never be be allowed have a nuclear weapon,’ he said.

And Trump backed up that vow with a threat:

‘Our missiles are big, powerful, accurate, lethal and fast,’ he said, sending a warning in nearly the same breath as an olive branch.

‘Under construction are many hypersonic missiles,’ he warned, standing amid a tableau of stern-faced military leaders.

Minutes later he offered an olive branch, urging European nations to make ‘a deal with Iran that makes the world a safer and more peaceful place’ and allows Iran to explore its ‘untapped potential’ as a mainstream trading partner.

‘We want you to have a future, and a great future,’ he told Iran’s people, claiming its military ‘appears to be standing down.’

President Donald Trump delivered a high-stakes address to the world on Wednesday, offering Iran peace if it abandons its nuclear ambitions but also threatening the use of hypersonic weapons if war follows

Talking peace and war: Donald Trump offered to ’embrace peace’ with Iran if it gives up its nuclear ambitions and its terrorism – but listed U.S. military capabilities

The president spoke in the Grand Foyer of the White House, speaking with the aid of a teleprompter in measured tones

Trump’s made-for-TV tableau included Secretary of Defense Mark Esper, Chairman of the Joint Chiefs of Staff Gen. Mark Milley and Vice President Mike Pence

Tightly-scripted: Donald Trump stuck to the teleprompter version of his address to the nation about Iran

No questions: Donald Trump left without taking any questions from reporters who had been brought into the room before his speech

Television entrance: Donald Trump enters to address the nation in the aftermath of missile strikes by Iran on a U.S. base in Iraq

The president’s audience-of-one was Iran Supreme Leader Ayatollah Ali Khamenei, the iron-fisted theocrat who is the mortal enemy of Israel and the United States

His remarks, watched live around the world, came after Tehran’s armies rained missiles down on Iraqi military installations where American troops have been stationed for more than 16 years.

‘No Americans were harmed in last night’s attack by the Iranian regime,’ the president said. ‘We suffered no casualties.’

Iranian state-run television claimed at least 20 U.S. servicemen and women were killed.

U.S. officials believe the missiles were deliberately fired into unpopulated areas, in what a senior official called a ‘heads-up bombing.’

The president spoke with the aid of tele-prompters in the Grand Foyer, the main entrance hall in the front of the White House.

He blasted Tehran’s ‘destructive and destabilizing behavior’ and said the days of Western patience ‘are over.’

Trump has long seen himself as a maverick loner on the world stage, unpredictable and unbothered by ruffling feathers overseas.

He boasts that his low approval ratings in foreign countries are an indication that he is focused on Americans’ welfare—not the priorities of real and nominal allies.

That approach could be tested as Iran and the U.S. creep toward what some, but not all, in the national security establishment see as an inevitable war.

The White House isn’t expecting one, the senior official said Wednesday: ‘This doesn’t have to end badly, and frankly right now we might be in the best position ever for diplomacy with Tehran.’

As he has in the past, the president trashed the Iran nuclear deal negotiated during the Obama administration along with Tehran and six other powers. He called the deal, which the administration already backed away from, ‘very defective’ noting that it ‘expires anyway.’

He called on other negotiating parties, including Great Britain, France, Germany, and Russia – to ‘break away from the remnants of the Iran deal.

At the same time, Trump did not completely foreclose negotiation. He called for a ‘deal with Iran that makes the world a more peaceful and safer place.’

Trump, who spoke to reporters but had yet to speak directly to the nation since ordering the killing of Soleimani, called the Iranian general ‘the world’s top terrorist,’ and said he was ‘personally responsible for some of the absolutely worst atrocities.’

‘Soleimani’s hands were drenched in both American and Iranian blood,’ Trump said. ‘He should have been terminated long ago. By removing Soleimani, we have sent a powerful message to terrorists: If you value your own life, you will not threaten the lives of our people,’ he added.

Trump announced that the U.S. would impose ‘powerful’ sanctions on the already heavily-sanctioned Iranian regime. But the White House did not immediately provide specifics. Treasury Secretary Steven Mnuchin was seen exiting the meeting Trump had with top military and security advisors moments before the speech.

‘The United States will immediately impose additional punishing economic sanctions on the Iranian regime. These powerful sanctions will remain until Iran changes its behavior,’ Trump said.

The Islamic Revolutionary Guard Corps fired on the Ain al-Asad airbase in western Iraq and Erbil International airport in the north in the early hours of Wednesday, but failed to kill a single US or Iraqi solider.

Ayatollah Ali Khamenei, speaking on Iranian TV shortly after the missiles were launched, described the strikes as ‘a slap’ and said they ‘are not sufficient (for revenge)’ while vowing further action to kick US troops out of the region.

But foreign minister Mohammad Javad Zarif said the attack was now ‘concluded,’ praising Iran’s ‘proportionate’ response and adding: ‘We do not seek escalation or war.’

Trump tweeted late Tuesday to say ‘so far so good’ as American forces assessed the damage and casualties.

Iranian television had tried to claim that 80 ‘American terrorists’ were killed, but that figure was quickly rubbished by Iraqi and US officials.

Images showed several missiles had either failed to explode on impact or else missed their targets. The remains of one was found near the town of Duhok, some 70 miles from Erbil air base, which was the intended target.

Tehran fired an ineffective missile strike at U.S. forces at Iraqi air bases after promising brutal revenge for Trump’s drone strike that killed General Qassem Soleimani (pictured), the architect of terror attacks that have killed hundreds of American servicemen and women

+49

Iran has fired 22 ballistic missiles at two Iraqi bases housing American troops in a revenge attack for the U.S. drone strike that killed top Iranian general Qassem Soleimani

+49

+49

The Ain al-Asad airbase in western Iraq that was visited by Donald Trump in December 2018 and the Erbil base in Iraqi Kurdistan were both struck by the missiles on Tuesday at about 5.20pm EST (1.20am local time)

It is thought Iran used Fatteh-110 and Qaim-1 ballistic missiles during the attack, which failed to kill any US or Iraqi troops (pictured, one of the missiles is launched in Iran)

Ayatollah Ali Khamenei (left) said the attack it is ‘not enough’ for revenge against the US, before Iraqi militia commander Qais al-Khazali (right) vowed to exact his own revenge for the killing of Abu Mahdi al-Muhandis

+

Iraqi security forces clear away pieces of shrapnel from the Ain al-Asad airbase after it was struck by ballistic missiles fired by Iran as part of operation ‘Martyr Soleimani’

+49

Initial reports indicate at least 15 missiles were fired at two American bases in Iraq, though officials said early warning systems sounded alarms at the Ain al-Asad base (pictured) allowing troops to scramble for cover

A man holds shrapnel from a missile launched by Iran on U.S.-led coalition forces on the outskirts of Duhok, in northern Iraq 70 miles from Erbil, following Iranian missile strikes

Wreckage of a missile that was fired at Ain al-Asad military base in western Iraq but failed to explode on impact

US officials said early warning systems sounded alarms at the Ain al-Asad base, allowing troops to scramble for cover

Iraq said 17 missiles were fired at the Ain al-Asad base, two of which failed to explode (pictured, unexploded wreckage)

In an attempt to talk-up the impact of the strikes, Iranian President Hassan Rouhani said they show ‘we don’t retreat in the face of America.’

‘If America has committed a crime… it should know that it will receive a decisive response,’ Rouhani said in a televised address. ‘If they are wise, they won’t take any other action at this juncture.’

It is thought Iran gave advanced warning of the strikes, after Iraq, Finland and Lithuania – which all had troops stationed at the bases which were targeted – all said they were informed in advance.

America said that ‘early warning systems’ detected the missile launches and sirens were sounded at the Asad base, allowing soldiers to seek shelter. It is not clear whether they were also informed by Iran.

Prominent analysts suggested Iran may have deliberately pulled its punches because they are fearful of the ‘disproportionate’ response threatened by Trump if US personnel were killed.

‘With the attacks, Tehran signalled its capacity and readiness to respond to US attacks, thus saving face, and yet they have been well targeted to avoid fatalities and thus avoid provoking Trump’s reaction,’ said Annalisa Perteghella of the Institute for International Political Studies in Milan.

President Donald Trump says ‘all is well’ and ‘so far so good’ as the damage and casualties continue to be assessed after Iran fired more than a dozen ballistic missiles at two Iraqi bases housing American troops

Iran’s foreign minister Javad Zarif called the attacks ‘self-defense’ but said they did ‘not seek escalation’ but would defend itself against further aggression

Hours after the launch, a Ukrainian Airlines Boeing 737 caught fire crashed near Tehran killing all 177 passengers and crew – including 63 Canadian and three Britons – amid fears it could have been caught up in the attack.

The Ukrainian embassy in Tehran initially stated that the crash had been caused by an engine failure rather than terrorism or a missile attack, but later deleted that claim.

Iran has blamed technical failure and an engine fire for the crash, after early saying the pilot had lost control during an engine fire.

If it emerges that Iran did shoot down the plane – either accidentally or on purpose – then it is likely to prompt a global response that will escalate tensions in the region even further.

Ukraine’s foreign ministry said of those killed, 82 were Iranian, 63 Canadian, 11 Ukrainian, three British, with the remainder hailing from Sweden, Afghanistan, and Germany.

The timing of the Iranian strikes – around 1.20am local time – occurred at the same time as the US drone strike which killed Soleimani.

Following the strikes, the Islamic Revolutionary Guard Corps warned any further strikes by America would be met with fresh attacks, and that any allied countries used as a base for such strikes would themselves become targets.

The Iraqi military said 22 missiles were fired in total – 17 at the Asad base, two of which failed to explode, and five more that struck Erbil International Airport. US officials put the total slightly lower at 15 – ten of which hit Asad, one which hit Erbil, four which failed in flight.

Iran said it had used Fatteh-110 ballistic missiles for the attack, though analysts said images of wreckage near the Aasd base also appears to show Qaim-1 ballistic missiles were used.

The Ain al-Asad airbase in western Iraq – visited by Trump in December 2018 – and Erbil base in Iraqi Kurdistan were struck by the missiles around 5.20pm EST Tuesday in an operation dubbed ‘Martyr Soleimani’ by Iran.

The Pentagon says the missiles were ‘clearly launched from Iran’ to target U.S. military and coalition forces in Iraq. A US official said there were no immediate reports of American casualties, though buildings were still being searched. Iraqi officials say there were no casualties among their forces either.

There are still fears for US forces in the region after Qais al-Khazali, a commander of Iran-backed Popular Mobilization Forces in Iraq, vowed to exact revenge for the killing of deputy-leader Abu Mahdi al-Muhandis.

‘The first Iranian response to the assassination of the martyr leader Soleimani took place,’ he tweeted. ‘Now is the time for the initial Iraqi response to the assassination of the martyr leader Muhandis.

‘And because the Iraqis are brave and zealous, their response will not be less than the size of the Iranian response, and this is a promise.’

+49

Supreme Leader Ayatollah Ali Khamenei said Iran had delivered a ‘slap in the face’ to American forces but added that missile strikes are ‘not enough’ and called for the US to be ‘uprooted’ from the region

+49

The Ayatollah spoke in a televised address early Wednesday during which he praised a ‘measured’ strike against the US, which he said embodied the spirit of slain general Soleimani

The Ain al-Asad airbase in western Iraq and the Erbil base in Iraqi Kurdistan were both struck by the missiles on Tuesday at about 5.30pm (EST)

President Trump and First Lady Melania visited the al-Asad airbase in western Iraq in December 2018. The airbase was targeted by Iran on Tuesday in a missile attack

Defense Secretary Mark Esper and Secretary of State Mike Pompeo were spotted arriving at the White House soon after news of the strikes broke

Iraqi security forces and citizens gather to inspect the site where missiles fired by Iran’s Revolutionary Guard Corps landed outside the Ain al-Asad airbase

Pieces of shrapnel are seen near the Ain al-Asad airbase after a missile strike by Iran

Members of Peshmerga fighters stand guard in center of Erbil in the aftermath of Iran’s launch of a number of missiles at bases in Iraq

Members of Kurdistan’s regional government attend a meeting to discuss security after Iranian missiles targeted Erbil International Airport early Wednesday

Britain, Australia, France, Poland, Denmark and Finland have confirmed that none of their troops stationed in Iraq were hurt in the attack, while calling for an end to hostilities and a return to talks.

European Commission President Ursula von der Leyen vowed the EU will ‘spare no effort’ in trying to save the nuclear deal that Iran signed with President Obama and was ripped up by Trump, sparking the current tensions.

China and Russia, both key Iranian allies, also warned against escalating strikes with Vladimir Dzhabarov, lawmaker with Russia’s upper house of parliament, warning the conflict could easily lead to a nuclear war.

The Syrian government, another key ally of Iran, has expressed full solidarity with Iran, saying Tehran has the right to defend itself ‘in the face of American threats and attacks.’

The foreign ministry said in a statement Wednesday that Syria holds the ‘American regime responsible for all the repercussions due to its reckless policy and arrogant mentality.’

Meanwhile Turkey, which is a NATO member but also has ties to Iran in Syria, said its foreign minister will visit Iraq on Thursday as part of diplomatic efforts to ‘alleviate the escalated tension’ in the region.

Iran’s Revolutionary Guards, which controls the country’s missile program, confirmed that they fired the rockets in retaliation for last week’s killing of Iranian general Qassem Soleimani.

They reported the operation’s name was ‘Martyr Soleimani’ and it took place just hours after the slain general’s funeral.

The rockets used in the attack, according to Iranian TV, were Fatteh-110 ballistic missiles, which have a range of 186 miles or 300km.

The Iranian air force has since deployed multiple fighter jets to patrol it airspace, according to reports – as Iran warned the U.S. and its allies in the region not to retaliate.

The Pentagon said it was still working to assess the damage.

Iranian missiles that blitzed Iraqi airbases can deliver a precision-guided 500lb warhead over a range of more than 180 miles

Two types of ballistic missiles were reportedly used to hit U.S. Military bases in Ain al-Asad in western Iraq and also around Erbil in Iraqi Kurdistan.

The majority of those used are believed to be the Fateh-110, which can travel 180 miles or 300km and have a payload of around 500lb.

Reports also suggest the Qiam-1 was also used, a short range ballistic missile produced by Iran which can travel 500 miles and carry 750lb warheads.

The Fateh-110 is an Iranian-designed, short-range, surface-to-surface ballistic missile that can be launched from any location.

While the Qiam-1 was specifically built to target U.S. bases in the Middle East, which have ‘encircled Iran’, according to Iranian sources.

When it was launched the Fateh-110 was described by Iranian defence minister Brigadier General Amir Hatami as ‘100-percent domestically made – agile, stealth, tactical (and) precision-guided’.

Both missiles are reported to have been fired from Tabriz and Kermanshah provinces in Iran.

‘In recent days and in response to Iranian threats and actions, the Department of Defense has taken all appropriate measures to safeguard our personnel and partners. These bases have been on high alert due to indications that the Iranian regime planned to attack our forces,’ a statement from the Pentagon read.

‘It is clear that these missiles were launched from Iran and targeted at least two Iraqi military bases hosting U.S. military and coalition personnel at al-Assad and Irbil. We are working on initial battle damage assessments.

‘As we evaluate the situation and our response, we will take all necessary measures to protect and defend U.S. personnel, partners, and allies in the region.’

The Islamic Revolutionary Guard Corps, a branch of the Iranian Armed Forces, reportedly said Iran’s supreme leader Ayatollah Khamenei was personally in the control center coordinating the attacks.

They also warned U.S. allies in the Middle East that they would face retaliation if America strikes back against any Iranian targets from their bases.

‘We are warning all American allies, who gave their bases to its terrorist army, that any territory that is the starting point of aggressive acts against Iran will be targeted,’ they said. It also threatened Israel.

Defense Secretary Mark Esper and Secretary of State Mike Pompeo were spotted arriving at the White House soon after news of the strikes broke.

South Carolina Senator Lindsey Graham said on Tuesday night that the missile strikes were an ‘act of war’ and said Trump had all the power he needed to act.

‘This is an act of war by any reasonable definition,’ Graham told Fox News’ Sean Hannity. ‘The President has all the authority he needs under Article II to respond.’

People stand near the wreckage after a Ukrainian plane carrying 177 passengers crashed near Imam Khomeini airport

Rescue workers in protective suits gather up the bodies of passengers who were killed in the Boeing 737 crash in Iran today

An aerial view of the crash site where rescuers searched the debris this morning with the cause of the crash still unclear

Mohammad Reza Kadkhoda-Zadeh (pictured), 40, has been named as the first British victim of the Ukrainian Airlines disaster

House Speaker Nancy Pelosi tweeted that the U.S., as well as the rest of the world, ‘cannot afford war’.

‘Closely monitoring the situation following bombings targeting U.S. troops in Iraq. We must ensure the safety of our servicemembers, including ending needless provocations from the Administration and demanding that Iran cease its violence. America & world cannot afford war,’ she tweeted.

After the strikes, Saeed Jalili – a former Iranian nuclear negotiator and foreign minister – posted a picture of the Islamic Republic’s flag on Twitter, appearing to mimic Trump who posted an American flag following the killing of Soleimani and others in the drone strike in Baghdad.

Ain al-Asad air base was first used by American forces after the 2003 U.S.-led invasion that toppled dictator Saddam Hussein, and later saw American troops stationed there amid the fight against the Islamic State group in Iraq and Syria. It houses about 1,500 U.S. and coalition forces.

About 70 Norwegian troops also were on the air base but no injuries were reported, Brynjar Stordal, a spokesperson for the Norwegian Armed Forces said.

The U.S. Federal Aviation Administration said on Tuesday it would ban U.S. carriers from operating in the airspace over Iraq, Iran, the Gulf of Oman and the waters between Iran and Saudi Arabia after the missile attack on U.S.-led forces.

Earlier on Tuesday, Defense Secretary Mark Esper said the United States should anticipate retaliation from Iran over the killing in Iraq of Soleimani.

‘I think we should expect that they will retaliate in some way, shape or form,’ Esper told a news briefing at the Pentagon, adding that such retaliation could be through Iran-backed proxy groups outside of Iran or ‘by their own hand.’

‘We’re prepared for any contingency. And then we will respond appropriately to whatever they do.’

Trump had also earlier told reporters about the prospect of an Iranian attack: ‘We’re totally prepared.’

‘They’re going to be suffering the consequences and very strongly,’ he said from the Oval Office during a meeting with Greek Prime Minister Kyriakos Mitsotakis.

Meanwhile, early reports of an attack at the al-Taji military base, just outside Baghdad, was later reported as a drill.

Local reports initially suggested that five rockets had struck the base after ‘shelter in place’ sirens were heard ringing out around the compound.

Sirens were also heard blaring out inside the U.S. consulate in Erbil, which was one of the bases struck in the missile attack.

+49

Iran said the attack, dubbed Operation Martyr Soleimani, was launched hours after the funeral service for General Qassem Soleimani (pictured) – who was killed in a US drone strike – had finished

+49

Mourners attend funeral and burial of General Soleimani in his hometown in Kerman early Wednesday morning

+49

People lower the coffin of Qassem Soleimani into his grave in the city of Kerman, central Iran

Mourners rush to lay their hands on the coffin of General Soleimani before it is lowered into a grave in the cit of Kerman

Was the Ukrainian jet brought down by an Iranian missile – or were the 176 people on board killed by a mechanical failure? Here are the five key theories

Theory one: Mechanical failure or pilot error

+49

Iranian authorities have said that initial investigations point to either an engine failure – or a catastrophic pilot error.

The three-year-old Boeing 737 jet came down just three minutes after take-off from Imam Khomeini International Airport.

Iranian officials said the pilot had lost control of the Boeing jet after a fire struck one of the plane’s engines, but said the crew had not reported an emergency and did not say what caused the fire.

Footage of the crash appears to show the plane streaking downwards with a small blaze on the wing, near its jet engines (pictured above on the ground).

But critics have questioned the Iranian account, calling it the ‘fastest investigation in aviation history’ – and said the Boeing 737 has a largely outstanding safety record with no recent history of an engine failure of this kind.

Ukrainian President Volodymyr Zelenskiy has instructed prosecutors to open criminal proceedings – a clear signal that he is unsure about Iran’s version of events.

His Government also revealed the plane was inspected just two days ago.

Theory two: Accidentally hit by an Iranian missile

The plane came down shortly after Iran launched its missile attacks Iraq with tens of ballistic weapons fired from the rogue state.

Photographs of the downed Ukrainian airlines jet show that the fuselage appears to be peppered with shrapnel damage.

Experts have said that an engine fire or pilot error does not explain those holes (pictured).

Ilya Kusa, a Ukrainian international affairs expert, said amid the US-Iranian tensions and said: ‘It is difficult not to connect the plane crash with the US-Iran confrontation. The situation is very difficult. One must understand that this happened shortly after Iran’s missile attacks on US military facilities’.

Just hours before the crash, the US Federal Aviation Administration had banned US airlines from flying over Iran, Iraq and the waters of the Persian Gulf due to the Middle East crisis.

This was due to the possibility of missiles flying towards Iraq – and airlines are still skirting the region as they head to and from Asia.

Theory three: Jet was deliberately brought down by a missile

+49

Video footage tweeted by the BBC‘s Iran correspondent, Ali Hashem, appeared to show the plane already burning in the sky before it crashed in a massive explosion.

It sparked speculation that the jet could have been shot down accidentally by nervous Iranian air defence soldiers, hours after Iran fired 22 ballistic missiles at US bases in retaliation for the killing of general Qassem Soleimani.

But there is a major question mark over whether Iran would shoot down a plane with so many of its own citizens on board.

Many of the world’s major airlines have stopped flying through or even near Iranian airspace as they cross the globe amid safety fears after US/Iran tensions boiled over in the past week.

Iran is a key ally of Vladimir Putin’sRussia, which grabbed Crimea from Ukraine and has been involved in an on-off conflict with its neighbour since 2014.

Russia has denied shooting down the ill-fated MH17 jet five years ago – but experts say otherwise with three Russians arrested over the disaster.

Theory four: An accidental drone strike

Experts have speculated that the Ukrainian aircraft could have collided with a military drone before crashing.

The drone may have smashed into the engine – or been sucked in – with the pilot unsighted because it was after dark.

This could cause an explosion and the fire seen as the plane hit the ground (pictured).

Experts said Iranian were in the air at the time – in case the US decided to fight back – and not always picked up by radar.

Russian military pilot Vladimir Popov said: ‘It could have been an unmanned reconnaissance aircraft, which are small in size and poorly visible on radars. A plane in a collision could get significant damage and even catch fire in the air.’

Theory five: Sabotage or a terror attack

Aviation experts have urged investigators to rule out whether the plane was brought down by terrorists or as an act of sabotage.

They say that while a flaming engine is highly unusual, the sudden loss of data communications from the plane is even more so.

This could be caused by a bomb, that blew up after the 737 took to the air, wrecking its systems.

An electronic jammer weapon that knocked out the plane’s controls could also explain it.

British expert Julian Bray said it ‘could be an altitude triggered device set to detonate during take off. Unusual that engine seen to be on fire before crash, points to catastrophic incident’ or being ‘deliberately brought down’.

He added that based on the footage pilot error looks ‘unlikely’.

Experts have said that if the black box is not recovered by Iranian security officials (pictured) from the wreckage it could point to it being a deliberate act.

After the crash the Ukrainian embassy in Tehran reported that the crash had been caused by an engine failure rather than terrorism – but this was later deleted on social media.

The strikes by Iran were a major escalation of tensions that have been rising steadily across the Mideast following months of threats and attacks after Trump’s decision to unilaterally withdraw America from Tehran’s nuclear deal with world powers.

Soleimani’s killing and Iran’s missile strikes also marked the first time in recent years that Washington and Tehran have attacked each other directly rather than through proxies in the region.

After the strikes, Saeed Jalili – a former Iranian nuclear negotiator – posted a picture of the Islamic Republic’s flag on Twitter, appearing to mimic Trump who posted an American flag following the killing of Soleimani and others in the drone strike in Baghdad

It raised the chances of open conflict erupting between the two nations, which have been foes since the days immediately following Iran’s 1979 Islamic Revolution.

The revenge attack came a mere few hours after crowds in Iran mourned Soleimani and as the U.S. continued to reinforce its own positions in the region and warned of an unspecified threat to shipping from Iran in the region’s waterways, crucial routes for global energy supplies.

U.S. embassies and consulates from Asia to Africa and Europe issued security alerts for Americans. The U.S. Air Force launched a drill with 52 fighter jets in Utah on Monday, just days after Trump threatened to hit 52 sites in Iran.

Meanwhile a stampede broke out Tuesday at Soleimani’s funeral in his hometown of Kerman and at least 56 people were killed and more than 200 were injured as thousands thronged the procession, Iranian news reports said.

There was no information about what set off the crush in the packed streets. Online videos showed only its aftermath: people lying apparently lifeless, their faces covered by clothing, emergency crews performing CPR on the fallen and onlookers wailing and crying out to God.

A procession in Tehran on Monday drew over one million people in the Iranian capital, crowding both main avenues and side streets.

Hossein Salami, Soleimani’s successor as leader of the Revolutionary Guard, addressed a crowd of supporters gathered at the coffin in a central square in Kernan.

He vowed to avenge Soleimani, saying: ‘We tell our enemies that we will retaliate but if they take another action we will set ablaze the places that they like and are passionate about’.

The al-Asad base for American and coalition troops (pictured above in December) was struck by missiles ‘clearly launched from Iran’, U.S. officials say

+49

The Erbil base in Iraqi Kurdistan, which provides facilities and services to at least hundreds of coalition personnel and CIA operatives, was also hit in the missile attack

President Trump’s speech on Iran

As long as I am President of the United States, Iran will never be allowed to have a nuclear weapon.

Good morning. I’m pleased to inform you: The American people should be extremely grateful and happy no Americans were harmed in last night’s attack by the Iranian regime. We suffered no casualties, all of our soldiers are safe, and only minimal damage was sustained at our military bases.

Our great American forces are prepared for anything. Iran appears to be standing down, which is a good thing for all parties concerned and a very good thing for the world.

No American or Iraqi lives were lost because of the precautions taken, the dispersal of forces, and an early warning system that worked very well. I salute the incredible skill and courage of America’s men and women in uniform.

For far too long — all the way back to 1979, to be exact — nations have tolerated Iran’s destructive and destabilizing behavior in the Middle East and beyond. Those days are over. Iran has been the leading sponsor of terrorism, and their pursuit of nuclear weapons threatens the civilized world. We will never let that happen.

Last week, we took decisive action to stop a ruthless terrorist from threatening American lives. At my direction, the United States military eliminated the world’s top terrorist, Qasem Soleimani. As the head of the Quds Force, Soleimani was personally responsible for some of the absolutely worst atrocities.

He trained terrorist armies, including Hezbollah, launching terrorist strikes against civilian targets. He fueled bloody civil wars all across the region. He viciously wounded and murdered thousands of U.S. troops, including the planting of roadside bombs that maim and dismember their victims.

Soleimani directed the recent attacks on U.S. personnel in Iraq that badly wounded four service members and killed one American, and he orchestrated the violent assault on the U.S. embassy in Baghdad. In recent days, he was planning new attacks on American targets, but we stopped him.

Soleimani’s hands were drenched in both American and Iranian blood. He should have been terminated long ago. By removing Soleimani, we have sent a powerful message to terrorists: If you value your own life, you will not threaten the lives of our people.

As we continue to evaluate options in response to Iranian aggression, the United States will immediately impose additional punishing economic sanctions on the Iranian regime. These powerful sanctions will remain until Iran changes its behavior.

In recent months alone, Iran has seized ships in international waters, fired an unprovoked strike on Saudi Arabia, and shot down two U.S. drones.

Iran’s hostilities substantially increased after the foolish Iran nuclear deal was signed in 2013, and they were given $150 billion, not to mention $1.8 billion in cash. Instead of saying “thank you” to the United States, they chanted “death to America.” In fact, they chanted “death to America” the day the agreement was signed.

Then, Iran went on a terror spree, funded by the money from the deal, and created hell in Yemen, Syria, Lebanon, Afghanistan, and Iraq. The missiles fired last night at us and our allies were paid for with the funds made available by the last administration. The regime also greatly tightened the reins on their own country, even recently killing 1,500 people at the many protests that are taking place all throughout Iran.

The very defective JCPOA expires shortly anyway, and gives Iran a clear and quick path to nuclear breakout. Iran must abandon its nuclear ambitions and end its support for terrorism. The time has come for the United Kingdom, Germany, France, Russia, and China to recognize this reality.

They must now break away from the remnants of the Iran deal -– or JCPOA –- and we must all work together toward making a deal with Iran that makes the world a safer and more peaceful place. We must also make a deal that allows Iran to thrive and prosper, and take advantage of its enormous untapped potential. Iran can be a great country.

Peace and stability cannot prevail in the Middle East as long as Iran continues to foment violence, unrest, hatred, and war. The civilized world must send a clear and unified message to the Iranian regime: Your campaign of terror, murder, mayhem will not be tolerated any longer. It will not be allowed to go forward.

Today, I am going to ask NATO to become much more involved in the Middle East process. Over the last three years, under my leadership, our economy is stronger than ever before and America has achieved energy independence. These historic accompliments [accomplishments] changed our strategic priorities. These are accomplishments that nobody thought were possible. And options in the Middle East became available. We are now the number-one producer of oil and natural gas anywhere in the world. We are independent, and we do not need Middle East oil.

The American military has been completely rebuilt under my administration, at a cost of $2.5 trillion. U.S. Armed Forces are stronger than ever before. Our missiles are big, powerful, accurate, lethal, and fast. Under construction are many hypersonic missiles.

The fact that we have this great military and equipment, however, does not mean we have to use it. We do not want to use it. American strength, both military and economic, is the best deterrent.

Three months ago, after destroying 100 percent of ISIS and its territorial caliphate, we killed the savage leader of ISIS, al-Baghdadi, who was responsible for so much death, including the mass beheadings of Christians, Muslims, and all who stood in his way. He was a monster. Al-Baghdadi was trying again to rebuild the ISIS caliphate, and failed.

Tens of thousands of ISIS fighters have been killed or captured during my administration. ISIS is a natural enemy of Iran. The destruction of ISIS is good for Iran, and we should work together on this and other shared priorities.

Finally, to the people and leaders of Iran: We want you to have a future and a great future — one that you deserve, one of prosperity at home, and harmony with the nations of the world. The United States is ready to embrace peace with all who seek it.

I want to thank you, and God bless America. Thank you very much. Thank you. Thank you.

Bonner was a director of MoneyWeek from 2003 to 2009.[4]

Works

Bonner co-authored Financial Reckoning Day: Surviving The Soft Depression of The 21st Century and Empire of Debt with Addison Wiggin. He also co-authored Mobs, Messiahs and Marketswith Lila Rajiva. The latter publication won the GetAbstract International Book Award for 2008.[5] He has previously co-authored two short pamphlets with British media historian, John Campbell, and with The Times former editor, Lord William Rees-Mogg, and has co-edited a book of essays with intellectual historian, Pierre Lemieux.[6]

In his two financial books, as well as in The Daily Reckoning, Bonner has argued that the financial future of the United States is in peril because of various economic and demographic trends, not the least of which is America’s large trade deficit. He claims that America’s foreign policy exploits are tantamount to the establishment of an empire, and that the cost of maintaining such an empire could accelerate America’s eventual decline. Bonner argues in his latest book that mob and mass delusions are part of the human condition.[citation needed]

Bonner warned in 2015 that the credit system, which has been the essential basis of the US economy since the 1950s, will inevitably fail, leading to catastrophic failure of the banking system.[7][8]

In June 2016, Bill Bonner, via his company Agora, paid for an advertisement on Reuters describing a new law that would not allow Americans to take money out of their own USA accounts. The ad reads: “New Law Cracks Down on Right to Use Cash. Americans are reporting problems taking their own money out of US banks.” The advertisement does not cite the law (the Foreign Account Tax Compliance Act or FATCA[9]) to which it refers.

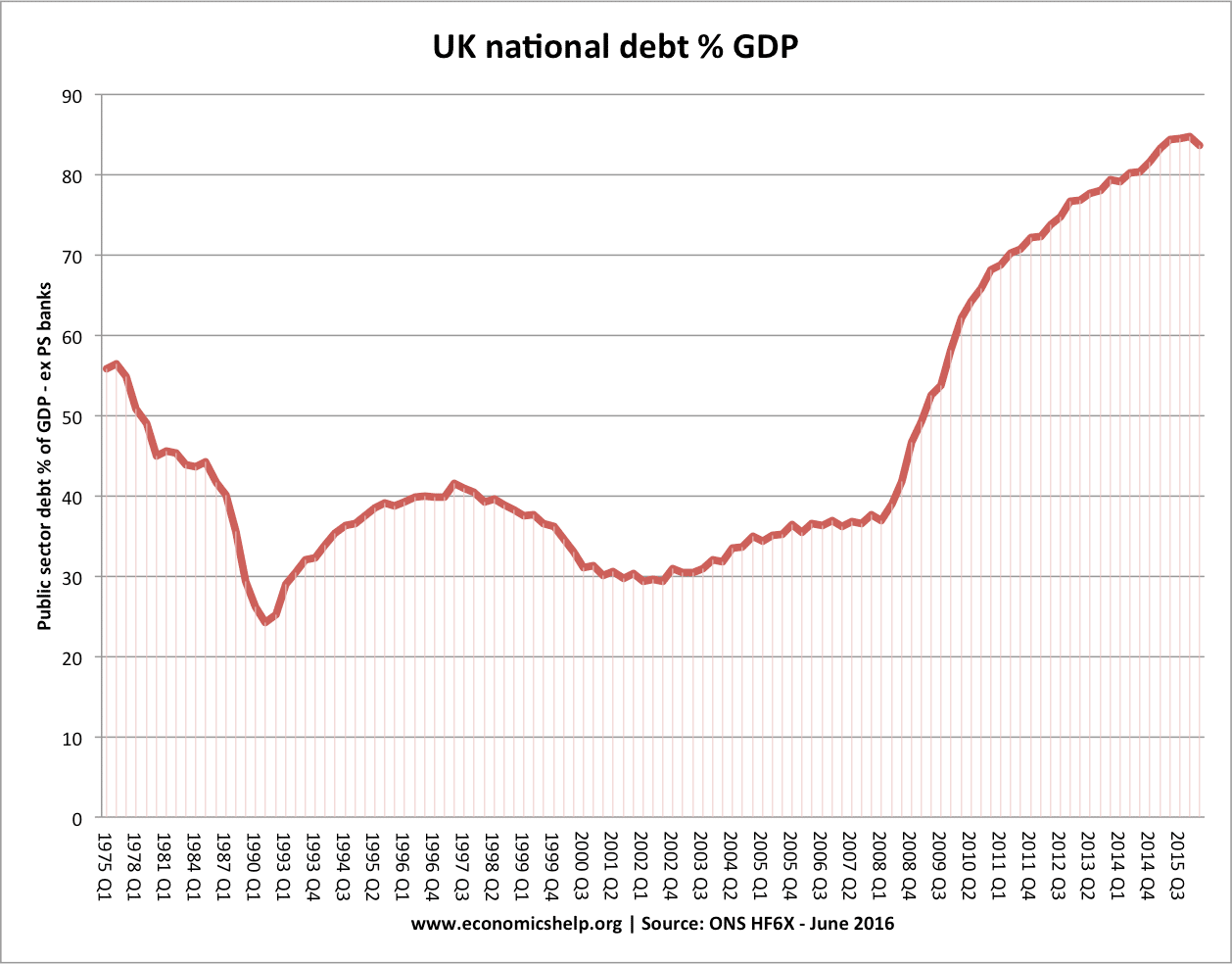

The national debt exceeded $21 trillion for the first time on Thursday, a little more than six months after it hit first $20 trillion on Sept. 8.

The national debt was $21.031 trillion on Thursday. The government releases total debt figures each business day, but it lags by one day.

Federal borrowing has been on the rise again since February, when Congress passed legislation to suspend the debt ceiling. That move allowed the government to borrow as much as it needs to fund the activities approved by Congress.

Under the law passed in February, the government will not face any borrowing limit until March 1, 2019. At its current pace, the government is on track to add at least $1 trillion to the national debt by then.

For example, the debt grew by more than half a trillion dollars in the six weeks since the debt ceiling was lifted on Feb. 9.

A large part of the national debt reflects the federal budget deficit, or the amount of spending above the revenues collected by the government. But the debt is rising faster than the amount of the budget deficit, as it also reflects things like federal lending for student loans and mortgage programs.

Peter G. Peterson Foundation President Michael Peterson said the milemarker is just the beginning, as Congress has just agreed to spend even more.

“Our national debt reached a staggering $21 trillion today, having grown by $1 trillion in just the past six months,” he said. “Worse yet, this unfortunate milestone has only just begun to include the effects of the recent fiscally irresponsible tax and spending legislation, which added more debt on top of an already unsustainable trajectory.”

Story 1: President Trump Delivers America First Address With Bilateral Trade Agreements With Nations That Want Free But Fair Trade At The Asia-Pacific Economic Cooperation (APEC) Summit in Da Nang, Vietnam — Videos —

Story 2: From Crying To Screaming — Big Lie Media Joins Lying Lunatic Left Losers — Sky Screaming — Trump Still President — Videos —

Story 3: Let Voters of Alabama Decide Who They Want For Their Senator — Alabama Republican Senate Candidate, Roy Moore, Denies Accusations Made in Washington Post Attack Article vs. Democratic Senate Candidate, Doug Jones, Supporter for Pro Abortion Planned Parenthood and Women Should Have The Right To Choose Killing Their Babies in The Womb — Denies Civil Rights Protection of Life To Babies Before Birth — Videos

Story 4: Remembering The Veterans in Music — Lili Marleen — We’ll Meet Again — Sky Pilot — We Gotta Get Out Of This Place — Paint it Black – – War — Where Have All the Flowers Gone? — Blowing In The Wind –Videos

Story 1: President Trump’s Address to South Korea’s National Assembly — Great Speech — Americans and Koreans Loved It — Every Breath You Take — Videos —

Story 2: President Trump Tells It Like It Is — Does Not Blame China For Hugh Trade Deficits But Past Administrations — Videos —

Story 3: Republican Party Senate Bill Wants To Delay Tax Cuts To 2019 Instead of Cutting Spending Now — Need New Political Party Advocating Balanced Budgets, Broad Based Consumption Tax,and Term Limits — Voters Will Stay Home Election Day, November 6, 2018 If Congress Does Not Completely Repeal Obamacare and Enact Fundamental Reform of Tax System — Videos —

Story 4: Alabama Republican Candidate for Senator, Roy Moore, Accused of Sexual Misconduct in 1979 — Desperate Democratic Dirt — Let The Voters of Alabama Decide — Accusations Are Not Evidence — Videos

Story 1: Communist Chinese Connection To Trade — Nuclear Proliferation — and — Terrorism (TNT) — Peace or War — China Must Destroy North Korea Nuclear Weapons and Missiles or Face The Consequences of Overthrow of Communist Party — U.S.Complete Embargo on All Chinese Trade and Investment —

Story 2: President Trump Meets With Japanese Prime Minster Shinzo Abe and President Moon Jai-in As U.S. Navy Flexes Air Power — All Options Are On The Table — Video —

Story 3: Saudi Arab On The Brink of War With Lebanon Controlled By Iran-backed Lebanese Shi‘ite group Hezbollah — Saudi Arab Blames Iran For Yemen Missile Attack — Purge and Roundup of Royal Prince Continues — Videos —

Story 1: Atheist Security Guard Dressed In Black and Wearing Body Armor, Devin Patrick Kelley, 26, Entered The First Baptist Church and Shoot and Killed 26, Including 8 Members of A Single Family with Pregnant Mother, Victim Range in Age From 18 Months to 77 Years and Wounded 20, in The Texas Small Town of Sutherland Springs, Population 400, A Nearby Neighbor, Stephen Willeford, 55, Shot Killer With His Rifle,Three Times, Twice in The Neck and Once in The Side, Killer Died of Wounds, After Brief High Speed Car Chase — The Times They Are A Changin — Blowing In The Wind — Videos

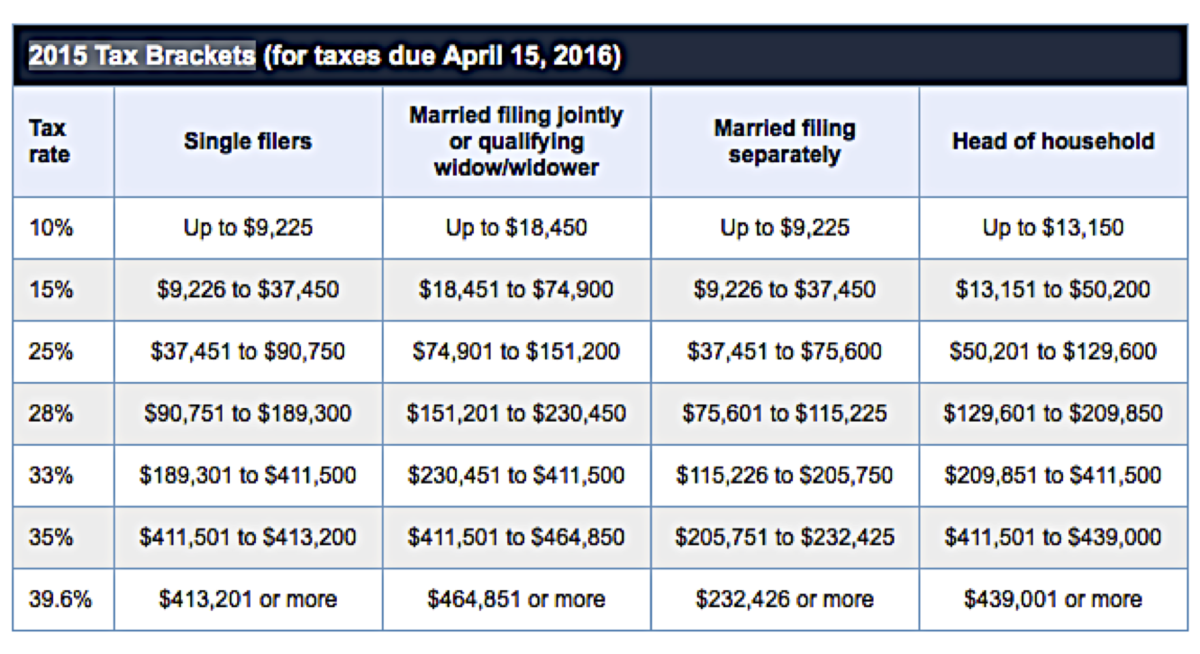

Story 1: Democrats (Liberal, Progressive & Socialist Wing) and Republicans (Liberal & Progressive Wing) of The Two Party Tyranny Are All Marxist Now — Big Government Bubble Tax Surcharge of 6% Increases Rate From 39.6% to 45.6% — Class Warfare — Eat The Rich — Videos — Part 2 of 2 —

Story 2: Republican Tax Cut Will Not Make America Great Again — Missing Is Real Government Spending Cuts That Results in A Balanced Budget By 2020 or 2024 — Spending Addiction Disorder (SAD) or Government Spending Obesity — Alive and Well — Videos —

Story 3: A Broad Based Consumption Tax Replacing The Current U.S. Income Tax System Along The Lines of The FairTax or Fair Tax Less With Generous Monthly Tax Prebates and Limiting Federal Government Expenditures to 90% of Taxes Collected Will Make America Great Again — Videos

Story 1: President Trump Nominates Fed Governor Jerome Powell To Chair Federal Reserve Board of Governors — Expect Continuation of Interventionist Easy Monetary Policy — More Money Creation or Quantitative Easing When Economy Enters Next Recession in 2018-2019 — Videos —

Part 1 of 2 — Story 2: No Tax Reform By Changing From Income Tax System to Broad Based Consumption Tax — The FairTax or Fair Tax Less — No Middle Class Tax Relief From Payroll Taxes — No Real Cuts in Federal Spending As Budget Deficits Rise with Rising National Debt and Unfunded Liabilities — Spending Addiction Disorder — Government Obesity — Crash Diet of Balanced Budgets Required — Videos

Story 1: Update of Radical Islamic Terrorist Jihadist Attack in New York City — President Trump “Send Him To Gitmo” as Enemy Combatant and Get Rid of Chain Migration and Diversity Lottery Immigration Program and Replace With Merit Based System of Immigration — Videos — Breaking —

Story 2: Trump Expected To Name Jerome Powell As Next Federal Reserve Chairman Replacing Chair Janet Yellen — A Dove or Continuation of Interventionist Easy Monetary Policy — Better Choice Was John Taylor — Taylor For Fed Chair and Powell for Vice Chair — Videos

Breaking Story 1: Rocket Man Kim Jong-Un Promises To Explode Hydrogen Bomb Over Pacific Ocean —

Story 2: The Democratic and Republican Party Failure To Completely Repeal Obamacare Including Repealing The Patient Protection and Affordable Care Act (ACA) and All Related Mandates, Regulations, Taxes, Spending and Subsidies — Obamacare Collapsing — Replace Obamacare With Free Enterprise Market Capitalism Health Insurance — Keep The Federal Government Out Of The Health Insurance and Health Care Business — Videos —

Story 3: Obama’s Secret Surveillance Spy State Scandal — Misuse of Intelligence Community For Political Purposes — Gross Abuse of Power and Political Conspiracy — Violation of Fourth Amendment — Videos —

Story 1: President Trump Signs Executive Order Targeting Institutions and People Doing Business With North Korea — Communist China Trades With and Enabled North Korea Nuclear Weapon and Missile Programs — Waiting For Embargo Banning All Trade and Investment in Communist China — Videos —

Story 2: Fed To Start Quantitative Tightening In October 2017 by Selling Some ($10 Billion Per Month or $120 Billion Per Year) of $4,500 Billion Bond Portfolio As U.S. Economy Slows in 2017? — Videos

Breaking and Developing — Story 1: 7.1 Richter Scale Earthquake Kills Over 200 In Mexico — Videos —

Story 2: Category 4 Hurricane Marie With 155 Miles Per Hour Winds, 10 Foot Flood Surge and 20 Plus Inches of Rainfall Turns Lights Out in Puerto Rico with Widespread Flooding and Damages — Videos —

Story 3: Yes The Obama Administration Was Wiretapping The Trump Campaign and Former Trump Campaign Manager Paul Manafort — Trump Was Right and Big Lie Media Lied Again — Obama Spying Scandal Bigger Than Watergate — Videos —

Story 4: Illegal Aliens Shout Down House Minority Leader Nancy Pelosi Calling Her A Liar — When Will American Citizens Shout Down President Trump Calling Him A Liar? … President Trump and Republican Party Want Touch Back Amnesty and Pathway to Citizenship For Illegal Aliens — Majority of American People Want All Immigration Laws Enforced — Deport and Remove All 30-60 Million Illegal Aliens In United States To Country of Origin — No Republican Re-importing of Illegal Aliens With Expedited Visas and Touch Back Amnesty and Pathway to Citizenship — Employ American Citizens Not Illegal Aliens — Videos

Story 1: President Trump United Nations Speech Names North Korea and Iran As Threats to World Peace and Critical of Those Nations (China) Who Trade With Them –Totally Destroy North Korea And The Rocket Man Mr. Kim — Videos —

Story 2: Major 7.1 Richter Scale Killer Earthquake Hits Central Mexico — 76 Miles Southwest of Mexico City Centered in Puebla state town of Raboso, — Damages and Collapses Buildings — Over 150 Deaths — Videos —

Story 3: Category 5 Hurricane Marie With Sustained Winds of 165 Miles Per Hour and Wind Gust 195 MPH Hits Puerto Rico, British and American Virgin Islands, Dominica, Dominican Republic, Guadeloupe — Videos

Story 1: Two Islamic Terrorists Arrested For London Train Attack — United Kingdom Threat Level Lowered From Critical To Severe — Elderly Couple Took In Several Hundred Forster Children Over The Years Including Two Suspected Terrorists — Trump: “Loser Terrorist” And “Sick And Demented” — 21-Year-Old Syrian Refugee Yahyah Farroukh Named Suspect — Videos —

Story 2: Trump Wants To Increase CIA Drone Attacks — Videos —

Story 3: Third Night Of Violence In St. Louis — Protesters And Vandals Damage Property With Over 120 Arrests And 11 Police Injured — Videos

Breaking Story 1: Radical Islamic Terrorist Attack — Improvised Bucket Bomb Device Explodes In United Kingdom Parson Green Tube Train Station in West London During Morning Rush Hour — 29 Injured None Seriously including Children — Threat Level Raised From Severe To Critical By Prime Minister May — Videos —

Story 2: North Korea Fires Another Ballistic Missile Over Japan — Videos —

Story 3: Conservative Commentator Ben Shapiro Allowed To Speak At University of California, Berkeley, Police Arrested Nine of The Protesters –Videos

Story 1: Did President Trump Betray His Supporters By Promising Citizenship or Pathway To Citizenship For Illegal Alien “Dreamers”? — Big Lie Media and Lying Lunatic Left Losers (Senate Democratic Leader Chuck Schumer and House Democratic Leader Nancy Pelosi ) Say They Have A Deal or Understanding and Rollover Republicans Support Trump (Senate Majority Leader Mitch McConnell and House Speaker Paul Ryan) — No Wall and No Deportation For 30-60 Million Illegal Aliens Including “Dreamers” — You Were Warned Not To Trust Trump — Rollover Republicans Want Touch-back Amnesty For Illegal Aliens — Hell No — Illegal Aliens Must Go — Trump Has 48 Hours To Confirm or Deny! — Political Suicide Watch Countdown — Videos

Story 1: American Collectivism (Resistance Is Futile) Vs. American Individualism (I Have Not Yet Begun To Fight!) — Federal Income, Capital Gains, Payroll,Estate And Gift Taxes, Budget Deficits, National Debt, Unfunded Liabilities, Democratic And Republican Parties, Two Party Tyranny Of The Warfare And Welfare State And American Empire Are The Past — The Future Is Fair Tax Less, Surplus Budgets, No Debts, No Unfunded Liabilities, And American Independence Party With A Peace And Prosperity Economy, Representative Constitutional American Republic Are The Future — Lead, Follow Or Get Out Of The Way — Those Without Power Cannot Defend Freedom — Videos

Breaking News — Story 1: Special Counsel Robert Mueller III Impanels Grand Jury for Russian Investigation and Alleged Russia/Trump Collusion Conspiracy Theory — Videos —

Story 2: Proposed Reforming American Immigration for Strong Employment (RAISE) Act will Expose Hypocrisy of Democrats and Republicans In Promoting Open Borders with 30-60 Million Illegal Invasion of United States Over The Last 30 Years and Rising Legal Immigration Instead of Protecting The American Worker and Middle Class — The Betrayal Of American People By The Political Elitist Establishment — Videos

Story 1: Vice-President On The Trump Doctrine In Speech Delivered From Estonia, Latvia, and Lithuania — Videos —

Story 2: President Trump Will Sign Sanctions Bill For Russia, North Korea, and Islamic Republic of Iran — Videos — Story 3: Washington War Fever with Neocon Republicans and Progressive Democrats United Against Russia — Masking Incompetency — Videos

Story 1bama Spy Scandal: Obama Administration Officials Including National Security Adviser Rice, CIA Director Brennan and United Nations Ambassador Power Spied On American People and Trump Campaign By Massive Unmasking Using Intelligence Community For Political Purposes — An Abuse of Power and Felonies Under U.S. Law — Videos

Story 1: Trump Targets Transgender Troops — No More Gender Reassignment Surgeries In Military and Veterans Hospital — Cuts Spending By Millions Per Year — What is Next? — No More Free Viagra — Tranny Boys/Girls No More — Videos —

Story 2: Senate Fails To Pass Senator Rand Paul’s Total Repeal Amendment — Tea Party Revival Calling For Primary Challenge Against Rollover Republican Senators Shelley Moore Capito of West Virginia, Susan Collins of Maine, Dick Heller of Nevada, John McCain of Arizona, Rob Portman of Ohio, Lamar Alexander of Tennessee and Lisa Murkowski of Alaska — All Republicans in Name Only — Really Big Government Democrats — Videos —

Story 3: Trump Rally in Ohio — Neither A Rally Nor A Movement Is Not A Political Party That Votes in Congress — New Viable and Winning American Independence Party Is What Is Needed –Videos

Story 1: Pence Breaks Tie — Senate Will Debate How To Proceed With Obamacare Repeal and Replace — Videos —

Story 2: Congress Overwhelming Passes New Sanctions on Russia, Iran and North Korea — Long Overdue — Videos —

Story 3: Trump Again Critical Of Attorney General Sessions Apparently For Not Prosecuting Leakers and Going After Clinton Foundation Crimes — What about Obama Administration’s Spying On Trump — An Abuse of Power Using Intelligence Community for Political Purposes — Will Trump Dump Sessions? If He Does Trump Will Start To Lose His Supporters in Talk Radio and Voter Base — Direct Deputy Attorney Rod Rosenstein To Fire Mueller — If He Won’t Fire Him — Fire Both Mueller and Rosenstein — Punish Your Enemies and Reward Your Friends President Trump! — “In Your Guts You Know He is Nuts” — Videos

What the Fed’s interest rate hike means for the economy

Stocks rally on Fed rate hike

Fed Hikes Rates, Signals More Coming

Is the Federal Reserve behind the curve?

What The Fed Rate Hike Means For Consumers

We Are Dangerously Close to a Recession

MARC FABER World Economy Grinding to a Halt. Don’t Trade With Leverage

Marc Faber : Volatility will pick up ‘massively’ , 30.1.2017

Marc Faber Warns : The Market is on the verge of a meaningful correction

Trump, China & World War 3 – Jim Rogers

The Whole System is Riddled With Corruption – James Dale Davidson Interview

Keiser Report: Rise of the Machines (E1043)

Keiser Report: Bloodletting Among Retailers (E1044)

David Stockman Interview Trump to Face Imploding Economy in 2017

David A. Stockman’s TEARS APART Trump’s Economic Plan

The Coming Big Freeze – Jim Rickards – The Daily Reckoning – Road to Ruin

James Rickards 2017 The Fed is Tapped Out & End Result is Ice Nine for Gold

AMTV Truth Exposed Prepare For The Imminent Global Economic Collapse 2017 Stock MARKET CRA

Fed rate hike: Central bank signals faster pace in 2017

Milton Friedman – The Federal Reserve Caused Great Depression

Milton Friedman on the Great Depression, Bank Runs & the Federal Reserve

Milton Friedman – Abolish The Fed

Milton Friedman: The Future of Freedom

Milton Friedman – Why Economists Disagree

Milton Friedman – The role of government in a free society

Milton Friedman Interview with Dallas Fed President Richard W. Fisher

Ep. 228: Inflation Finally Rears Its Head

What happens when the Fed raises rates

How Interest Rates Affect the Market

When Interest Rates Rise: Winners and Losers

ECONOMIC COLLAPSE: Trump to Declare Bankruptcy on U.S.

What’s all the Yellen About? Monetary Policy and the Federal Reserve: Crash Course Economics #10

The Federal Reserve Explained in 3 Minutes

Quantitative Easing Explained

The Collapse of The American Dream Explained in Animation

Who Controls the Money Controls the World

The Story of Your Enslavement

Financial Balance

“The Bernanke” explains Financial Repression

Financial Repression

Carmen Reinhart: Financial Repression Requires A Captive Audience | McAlvany Commentary

50 YEAR OLD CARTOON PREDICTS THE FUTURE !!! NWO !!!

Yellen Calms Fears Fed’s Policy Trigger Finger Is Getting Itchy

by Rich Miller, Christopher Condon , and Jeanna Smialek

March 15, 2017, 1:00 PM CDT March 15, 2017, 5:02 PM CDT

Policy makers still project three total rate hikes for 2017

FOMC sticks with ‘gradual’ plan for removing accommodation

Fed Raises Benchmark Lending Rate a Quarter Point

Federal Reserve Chair Janet Yellen sought to reassure investors that the central bank’s latest interest-rate increase wasn’t a paradigm shift to a trigger-happy policy driven by fears of faster inflation.

Speaking to reporters after the Fed’s quarter percentage-point move on Wednesday, Yellen said the central bank was willing to tolerate inflation temporarily overshootingits 2 percent goal and that it intended to keep its policy accommodative for “some time.”

“The simple message is the economy’s doing well. We have confidence in the robustness of the economy and its resilience to shocks,” she said.

As a result, the Fed is sticking with its policy of gradually raising interest rates, Yellen said. In their first forecasts in three months, Fed policy makers penciled in two more quarter-point rate increases this year and three in 2018, unchanged from their projections in December.

Today’s decision “does not represent a reassessment of the economic outlook or of the appropriate course for monetary policy,” the Fed chief said.

Speculation of a more aggressive Fed had mounted in recent days after a host of central bank officials, including Yellen herself, went out of their way to telegraph to financial markets that a rate hike was imminent. The expectations were further fueled by news of rising inflation.

Stocks Advance

Stocks rose and bond yields fell as investors viewed the statement from the Federal Open Market Committee and Yellen’s remarks afterward as a sign that the Fed isn’t in a hurry to remove monetary stimulus. The FOMC raised the target range for the federal funds rate to 0.75 percent to 1 percent, as expected, but Yellen’s lack of urgency to snuff out inflation was a surprise.

R.J. Gallo, a fixed-income investment manager at Federated Investors in Pittsburgh, said the chorus of Fed speakers before this meeting led investors to expect a move up in the number of projected rate hikes this year, and even upgrades by Fed officials in the levels of inflation and growth they anticipated.

None of that materialized.

“You didn’t get any of those things,” Gallo said, which explains why Treasury yields quickly dropped after the Fed released the FOMC statement and a new set of economic projections. “The expectation that Fed was getting more hawkish had to come out of the market.”

The U.S. economy has mostly met the central bank’s goals of full employment and stable prices, and may get further support if President Donald Trump delivers promised fiscal stimulus. Investor and business confidence has soared since Trump won the presidency in November, buoyed by his vows to cut taxes, lift infrastructure spending and ease regulations.

Still, the data don’t show an economy that’s heating up rapidly — a point Yellen herself made after the third rate hike since the 2007-2009 recession ended. In fact, the economy may have “more room to run,” she said.

Stronger business and consumer confidence hasn’t yet translated into increased investment and spending, said Yellen.

“It’s uncertain just how much sentiment actually impacts spending decisions, and I wouldn’t say at this point that I have seen hard evidence of any change in spending decisions,” said the Fed Chair. “Most of the business people that we’ve talked to also have a wait-and-see attitude.”

Retail sales in February grew at the slowest pace since August, a government report showed earlier Wednesday. The Atlanta Fed’s model for GDP predicts an expansion of 0.9 percent in the first quarter, less than a third the pace Trump is aiming for.

Fiscal Stimulus

Asked about the potential for a fiscal boost, Yellen made clear the Fed is still waiting for more concrete policy plans to emerge from the Trump administration before adapting monetary policy in reaction.

“There is great uncertainty about the timing, the size and the character of policy changes that may be put in place,” Yellen said. “I don’t think that’s a decision or set of decisions that we need to make until we know more about what policy changes will go into effect.”

Yellen disputed suggestions that the Fed was on a collision course with the Trump administration over its plans to foster faster economic growth through tax cuts and deregulation. “We would welcome stronger economic growth in the context of price stability,” she said.

She said she had met Trump briefly and had gotten together a couple of times with Treasury Secretary Steven Mnuchin to discuss the economy and financial regulation.

Further underscoring their lack of urgency, Fed officials repeated a commitment to maintain their balance-sheet reinvestment policy until rate increases were well under way. Yellen said officials had discussed the process of reducing the balance sheet gradually, but had made no decisions and would continue to debate the topic.

Policy makers forecast inflation will reach 1.9 percent in the fourth quarter this year, and 2 percent in both 2018 and 2019, according to quarterly median estimates released with the FOMC statement. The Fed’s preferred measure of inflation rose 1.9 percent in the 12 months through January, just shy of its target.

Yellen pointed out, though, that core inflation continues to run somewhat further below 2 percent. That rate, which strips out food and energy costs, stood at 1.7 percent in January. The Fed’s new forecast for the core rate at the end of this year edged up to 1.9 percent, from 1.8 percent in December.

“The committee will carefully monitor actual and expected inflation developments relative to its symmetric inflation goal,” the Fed said. Discussing the word symmetric in the statement, Yellen said during her press conference that the Fed was not shooting to push inflation over 2 percent but recognized that it could temporarily go above it. Two percent is a target, she reiterated, not a ceiling.

By Evan Tarver | Updated March 10, 2017 — 3:35 PM EST

SHARE

Changes in the federal funds rate will always affect the U.S. dollar. When the Federal Reserve increases the federal funds rate, it normally reduces inflationary pressure and works to appreciate the dollar.

Since June 2006, however, the Fed has maintained a federal funds rate of close to 0%. In the wake of the 2008 financial crisis, the federal funds rate fluctuated between 0-0.25%, and is now 0.75%.

The Fed used this monetary policy to help achieve maximum employment and stable prices. Now that the 2008 financial crisis has largely subsided, the Fed will look to increase interest rates to continue to achieve employment and to stabilize prices.

Inflation of the U.S. Dollar

The best way to achieve full employment and stable prices is to set the inflation rate of the dollar at 2%. In 2011, the Fed officially adopted a 2% annual increase in the price index for personal consumption expenditures as its target. When the economy is weak, inflation naturally falls; when the economy is strong, rising wages increase inflation. Keeping inflation at a growth rate of 2% helps the economy grow at a healthy rate.

Adjustments to the federal funds rate can also affect inflation in the United States. The Fed controls the economy by increasing interest rates when the economy is growing too fast. This encourages people to save more and spend less, reducing inflationary pressure. Conversely, when the economy is in a recession or growing too slowly, the Fed reduces interest rates to stimulate spending, which increases inflation.

During the 2008 financial crisis, the low federal funds rate should have increased inflation. Over this period, the federal funds rate was set near 0%, which encouraged spending and would normally increase inflation.

However, inflation is still well below the 2% target, which is contrary to the normal effects of low interest rates. The Fed cites one-off factors, such as falling oil prices and the strengthening dollar, as the reasons why inflation has remained low in a low interest environment.

The Fed believes that these factors will eventually fade and that inflation will increase above the target 2%. To prevent this eventual increase in inflation, hiking the federal funds rate reduces inflationary pressure and cause inflation of the dollar to remain around 2%.

Appreciation of the U.S. Dollar

Increases in the federal funds rate also result in a strengthening of the U.S. dollar. Other ways that the dollar can appreciate include increases in average wages and increases in overall consumption. However, although jobs are being created, wage rates are stagnant.

Without an increase in wage rates to go along with a strengthening job market, consumption won’t increase enough to sustain economic growth. Additionally, consumption remains subdued due to the fact that the labor force participation rate was close to its 35-year low in 2015. The Fed has kept interest rates low because a lower federal funds rate supports business expansions, which leads to more jobs and higher consumption. This has all worked to keep appreciation of the U.S. dollar low.

However, the U.S. is ahead of the other developed markets in terms of its economic recovery. Although the Fed raises rates cautiously, the U.S. could see higher interest rates before the other developed economies.

Overall, under normal economic conditions, increases in the federal funds rate reduce inflation and increase the appreciation of the U.S. dollar.

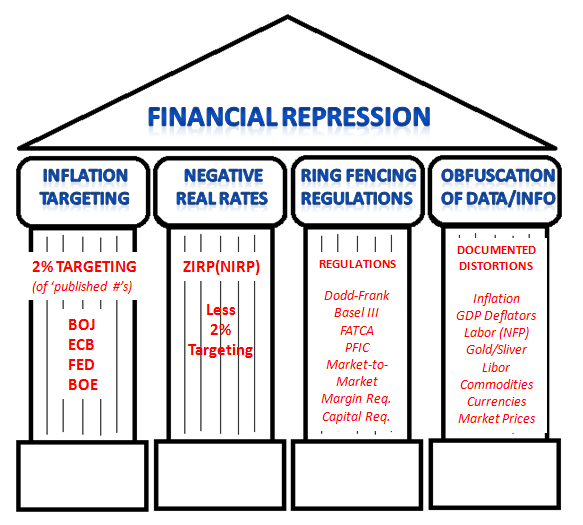

Not to be confused with economic repression, a type of political repression.

Financial repression refers to “policies that result in savers earning returns below the rate of inflation” in order to allow banks to “provide cheap loans to companies and governments, reducing the burden of repayments”.[1] It can be particularly effective at liquidating government debtdenominated in domestic currency.[2] It can also lead to a large expansions in debt “to levels evoking comparisons with the excesses that generated Japan’s lost decade and the Asian financial crisis” in 1997.[1]

Creation or maintenance of a captive domestic market for government debt, achieved by requiring banks to hold government debt via capital requirements, or by prohibiting or disincentivising alternatives.

Government restrictions on the transfer of assets abroad through the imposition of capital controls.

These measures allow governments to issue debt at lower interest rates. A low nominal interest rate can reduce debt servicing costs, while negative real interest rates erodes the real value of government debt.[5] Thus, financial repression is most successful in liquidating debts when accompanied by inflation and can be considered a form of taxation,[6] or alternatively a form of debasement.[7]

The size of the financial repression tax for 24 emerging markets from 1974 to 1987. Their results showed that financial repression exceeded 2% of GDP for seven countries, and greater than 3% for five countries. For five countries (India, Mexico, Pakistan, Sri Lanka, and Zimbabwe) it represented approximately 20% of tax revenue. In the case of Mexico financial repression was 6% of GDP, or 40% of tax revenue.[8]

Financial repression is categorized as “macroprudential regulation“—i.e., government efforts to “ensure the health of an entire financial system.[2]

Examples

After World War II

Financial repression “played an important role in reducing debt-to-GDP ratios after World War II” by keeping real interest rates for government debt below 1% for two-thirds of the time between 1945 and 1980, the United States was able to “inflate away” the large debt (122% of GDP) left over from the Great Depression and World War II.[2] In the UK, government debt declined from 216% of GDP in 1945 to 138% ten years later in 1955.[9]

China

China‘s economic growth has been attributed to financial repression thanks to “low returns on savings and the cheap loans that it makes possible”. This has allowed China to rely on savings-financed investments for economic growth. However, because low returns also dampens consumer spending, household expenditures account for “a smaller share of GDP in China than in any other major economy”.[1] However, as of December 2014, the People’s Bank of China “started to undo decades of financial repression” and the government now allows Chinese savers to collect up to a 3.3% return on one-year deposits. At China’s 1.6% inflation rate, this is a “high real-interest rate compared to other major economies”.[1]

After the 2008 economic recession

In a 2011 NBER working paper, Carmen Reinhart and Maria Belen Sbrancia speculate on a possible return by governments to this form of debt reduction in order to deal with high debt levels following the 2008 economic crisis.[5]

Critics[who?] argue that if this view was true, investors (i.e., capital-seeking parties) would be inclined to demand capital in large quantities and would be buying capital goods from this capital. This high demand for capital goods would certainly lead to inflation and thus the central banks would be forced to raise interest rates again. As a boom pepped by low interest rates fails to appear these days in industrialized countries, this is a sign that the low interest rates seem to be necessary to ensure an equilibrium on the capital market, thus to balance capital-supply—i.e., savers—on one side and capital-demand—i.e., investors and the government—on the other. This view argues that interest rates would be even lower if it were not for the high government debt ratio (i.e., capital demand from the government).

Free-market economists argue that financial repression crowds out private-sector investment, thus undermining growth. On the other hand, “postwar politicians clearly decided this was a price worth paying to cut debt and avoid outright default or draconian spending cuts. And the longer the gridlock over fiscal reform rumbles on, the greater the chance that ‘repression’ comes to be seen as the least of all evils”.[11]

Also, financial repression has been called a “stealth tax” that “rewards debtors and punishes savers—especially retirees” because their investments will no longer generate the expected return, which is income for retirees.[10][12] “One of the main goals of financial repression is to keep nominal interest rates lower than they would be in more competitive markets. Other things equal, this reduces the government’s interest expenses for a given stock of debt and contributes to deficit reduction. However, when financial repression produces negative real interest rates (nominal rates below the inflation rate), it reduces or liquidates existing debts and becomes the equivalent of a tax—a transfer from creditors (savers) to borrowers, including the government.”[2]

The interest rate that the borrowing bank pays to the lending bank to borrow the funds is negotiated between the two banks, and the weighted average of this rate across all such transactions is the federal funds effective rate.

The federal funds target rate is determined by a meeting of the members of the Federal Open Market Committee which normally occurs eight times a year about seven weeks apart. The committee may also hold additional meetings and implement target rate changes outside of its normal schedule.

Financial Institutions are obligated by law to maintain certain levels of reserves, either as reserves with the Fed or as vault cash. The level of these reserves is determined by the outstanding assets and liabilities of each depository institution, as well as by the Fed itself, but is typically 10%[4] of the total value of the bank’s demand accounts (depending on bank size). In the range of $9.3 million to $43.9 million, for transaction deposits (checking accounts, NOWs, and other deposits that can be used to make payments) the reserve requirement in 2007-2008 was 3 percent of the end-of-the-day daily average amount held over a two-week period. Transaction deposits over $43.9 million held at the same depository institution carried a 10 percent reserve requirement.

For example, assume a particular U.S. depository institution, in the normal course of business, issues a loan. This dispenses money and decreases the ratio of bank reserves to money loaned. If its reserve ratio drops below the legally required minimum, it must add to its reserves to remain compliant with Federal Reserve regulations. The bank can borrow the requisite funds from another bank that has a surplus in its account with the Fed. The interest rate that the borrowing bank pays to the lending bank to borrow the funds is negotiated between the two banks, and the weighted average of this rate across all such transactions is the federal funds effective rate.

The nominal rate is a target set by the governors of the Federal Reserve, which they enforce by open market operations and adjusting the interest paid on required and excess reserve balances. That nominal rate is almost always what is meant by the media referring to the Federal Reserve “changing interest rates.” The actual federal funds rate generally lies within a range of that target rate, as the Federal Reserve cannot set an exact value through open market operations.

Another way banks can borrow funds to keep up their required reserves is by taking a loan from the Federal Reserve itself at the discount window. These loans are subject to audit by the Fed, and the discount rate is usually higher than the federal funds rate. Confusion between these two kinds of loans often leads to confusion between the federal funds rate and the discount rate. Another difference is that while the Fed cannot set an exact federal funds rate, it does set the specific discount rate.

The federal funds rate target is decided by the governors at Federal Open Market Committee (FOMC) meetings. The FOMC members will either increase, decrease, or leave the rate unchanged depending on the meeting’s agenda and the economic conditions of the U.S. It is possible to infer the market expectations of the FOMC decisions at future meetings from the Chicago Board of Trade (CBOT) Fed Funds futures contracts, and these probabilities are widely reported in the financial media.

Applications

Interbank borrowing is essentially a way for banks to quickly raise money. For example, a bank may want to finance a major industrial effort but may not have the time to wait for deposits or interest (on loan payments) to come in. In such cases the bank will quickly raise this amount from other banks at an interest rate equal to or higher than the Federal funds rate.

Raising the federal funds rate will dissuade banks from taking out such inter-bank loans, which in turn will make cash that much harder to procure. Conversely, dropping the interest rates will encourage banks to borrow money and therefore invest more freely.[5] This interest rate is used as a regulatory tool to control how freely the U.S. economy operates.

By setting a higher discount rate the Federal Bank discourages banks from requisitioning funds from the Federal Bank, yet positions itself as a lender of last resort.