Archive for November 4th, 2013

Wall Street Journal On Obamacare: 79.8 Million Could Lose Coverage With Employer With (18 Million to 50 Million Actually Losing Coverage) — Edie Littlefield Sundby Loses Great Health Insurance Plan and Doctor Because of Obamacare — Shame On Obama — Videos

Pronk Pops Show 161: November 4, 2013

Pronk Pops Show 160: November 1, 2013

Pronk Pops Show 159: October 31, 2013

Pronk Pops Show 158: October 30, 2013

Pronk Pops Show 157: October 28, 2013

Pronk Pops Show 156: October 25, 2013

Pronk Pops Show 155: October 24, 2013

Pronk Pops Show 154: October 23, 2013

Pronk Pops Show 153: October 21, 2013

Pronk Pops Show 152: October 18, 2013

Pronk Pops Show 151: October 17, 2013

Pronk Pops Show 150: October 16, 2013

Pronk Pops Show 149: October 14, 2013

Pronk Pops Show 148: October 11, 2013

Pronk Pops Show 147: October 10, 2013

Pronk Pops Show 146: October 9, 2013

Pronk Pops Show 145: October 8, 2013

Pronk Pops Show 144: October 7, 2013

Pronk Pops Show 143: October 4 2013

Pronk Pops Show 142: October 3, 2013

Pronk Pops Show 141: October 2, 2013

Listen To Pronk Pops Podcast or Download Show 158-161

Listen To Pronk Pops Podcast or Download Show 151-157

Listen To Pronk Pops Podcast or Download Show 143-150

Listen To Pronk Pops Podcast or Download Show 135-142

Listen To Pronk Pops Podcast or Download Show 131-134

Listen To Pronk Pops Podcast or Download Show 124-130

Listen To Pronk Pops Podcast or Download Shows 121-123

Listen To Pronk Pops Podcast or Download Shows 118-120

Listen To Pronk Pops Podcast or Download Shows 113 -117

Listen To Pronk Pops Podcast or Download Show 112

Listen To Pronk Pops Podcast or Download Shows 108-111

Listen To Pronk Pops Podcast or Download Shows 106-108

Listen To Pronk Pops Podcast or Download Shows 104-105

Listen To Pronk Pops Podcast or Download Shows 101-103

Listen To Pronk Pops Podcast or Download Shows 98-100

Listen To Pronk Pops Podcast or Download Shows 94-97

Listen To Pronk Pops Podcast or Download Shows 93

Listen To Pronk Pops Podcast or Download Shows 92

Listen To Pronk Pops Podcast or Download Shows 91

Listen To Pronk Pops Podcast or Download Shows 88-90

Listen To Pronk Pops Podcast or Download Shows 84-87

Listen To Pronk Pops Podcast or Download Shows 79-83

Listen To Pronk Pops Podcast or Download Shows 74-78

Listen To Pronk Pops Podcast or Download Shows 71-73

Listen To Pronk Pops Podcast or Download Shows 68-70

Listen To Pronk Pops Podcast or Download Shows 65-67

Listen To Pronk Pops Podcast or Download Shows 62-64

Listen To Pronk Pops Podcast or Download Shows 58-61

Listen To Pronk Pops Podcast or Download Shows 55-57

Listen To Pronk Pops Podcast or Download Shows 52-54

Listen To Pronk Pops Podcast or Download Shows 49-51

Listen To Pronk Pops Podcast or Download Shows 45-48

Listen To Pronk Pops Podcast or Download Shows 41-44

Listen To Pronk Pops Podcast or Download Shows 38-40

Listen To Pronk Pops Podcast or Download Shows 34-37

Listen To Pronk Pops Podcast or Download Shows 30-33

Listen To Pronk Pops Podcast or Download Shows 27-29

Listen To Pronk Pops Podcast or Download Shows 17-26

Listen To Pronk Pops Podcast or Download Shows 16-22

Listen To Pronk Pops Podcast or Download Shows 10-15

Listen To Pronk Pops Podcast or Download Shows 01-09

Segment 0: Wall Street Journal On Obamacare: 79.8 Million Could Lose Coverage With Employer With (18 Million to 50 Million Actually Losing Coverage) — Edie Littlefield Sundby Loses Great Health Insurance Plan and Doctor Because of Obamacare — Shame On Obama — Videos

Obamacare sticker shock!

By Raymond Thomas Pronk

\

\

While gasoline prices may be going down, premiums, deductibles and co-payments for health insurance plans are skyrocketing.

Beginning Jan.1 all individual and group employer-provided health insurance must comply with the provisions of the Patient Protection and Affordable Care Act, commonly referred to as Obamacare.

More than 156 million Americans have their health insurance plans provided by their employers and another 25 million purchase their health insurance in the individual market, according to the Congressional Budget Office.

More than 60 million people age 65 and older and those younger with disabilities qualify for Medicare, a social insurance program that pays on average less than 50 percent of their health care costs. The balance of their health care costs must be paid for by the individual or the individual’s supplemental insurance.

More than 60 million Americans who are poor qualify for Medicaid, a government insurance program jointly funded by federal and state governments for individuals of all ages whose income and resources are insufficient to pay for health care. Obamacare expanded Medicaid coverage to those earning less than 138 percent of the federal poverty line (about $15,000 for an individual and $32,500 for a family of four). Twenty-four states have opted out of the Medicaid expansion, including Texas.

Those who do not qualify for Medicaid because their earned income is higher than the federal poverty line may qualify for subsidies or credits paid for by taxpayers if they purchase a plan from one of the insurance companies offering them on the new health insurance exchanges.

Most individuals and small group employers and their employees cannot keep their existing health insurance plans because of Obamacare. They are shocked by the high premiums, deductibles and co-payments of the new plans offered by insurance companies to replace their existing health insurance plans.

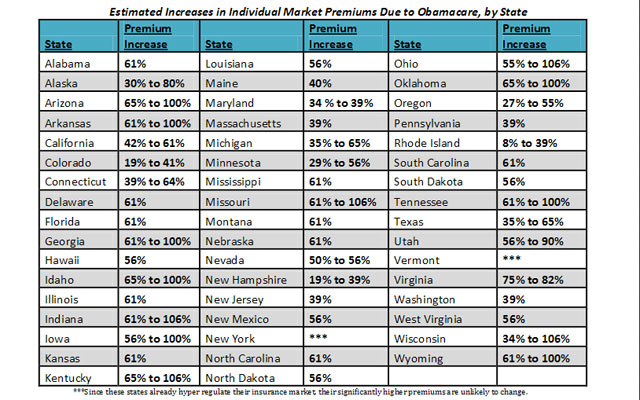

Credit: Texas Public Policy Foundation

One reason the premiums and deductibles for non-grandfathered (not in existence on March 23, 2010) individual and small group employer (employers with 50 or fewer employees) health care insurance plans are significantly increasing is Obamacare requires the insurance companies to offer a minimum core package of items and services referred to as Essential Health Benefits (EHB). The only plans not required to have EHB are fully insured large group plans, self-funded administrative services only plans and grandfathered plans.

These essential health benefits fall into 10 categories: ambulatory patient services, emergency services, hospitalization, laboratory services, maternity and newborn care, mental health services and addiction treatment, rehabilitative services and devices, pediatric services, prescription drugs, preventive and wellness services and chronic disease treatment. These EHBs must be included for plans offered both outside and inside the Health Insurance Marketplace such as those plans you find on the website healthcare.gov.

A second reason the premiums, deductibles and co-payments for non-grandfathered health insurance plans are increasing is that individuals with pre-existing conditions cannot be denied coverage and the plans cannot have a maximum lifetime limit for medical expenses.

Millions of Americans, because of their age, gender, lifestyle, marital status and religion, do not need maternity care and newborn care, mental health services and addiction treatment, pediatric services, abortions and contraceptives. These Americans were satisfied with and could afford their existing health insurance plans and wanted to keep them.

Americans believed Obama when he repeatedly said, “If you like your doctor, you will be able to keep your doctor, period. If you like your health care plan, you’ll be able to keep your health care plan, period. No one will take it away, no matter what.”

While in theory they could keep their plans under the Section 1251 “grandfather” provision of the Affordable Care Act, the regulations from the Obama administration interpreted this provision so strictly as to prevent most plans from being grandfathered.

Now the American people are learning from various news reports that the Obama administration officials knew in July 2010, when it published on page 34,522 of the Federal Register, that “The Departments’ mid-range estimate is that 66 percent of small employer plans and 45 percent of large employer plans will relinquish their grandfather status by the end of 2013.” This represents about 93 million Americans facing cancellation of their existing plans because of Obamacare.

A sure way for a president to lose the trust of the American people is to misinform them about something they must pay for, such as the premiums, deductibles and co-payments for their health insurance plans.

Obama broke his promise to the American people and as a result his presidential job approval poll numbers have plummeted from an all-time high of 68 percent in Jan. 22-24, 2009 to a low of 39 percent on Nov.5, according to Gallup.

Instead of making health insurance more affordable, Obamacare has made it more expensive for more than 181 million Americans who are now in sticker shock.

Steve Moore: ObamaCare Is Why Employers Are Dropping Health Plans

Avik Roy on Obamacare’s Cancellations of Employer-Sponsored Insurance 2013-10-31

Health Care News WSJ NBC Poll Most Americans Don’t Trust ObamaCare

RPT: 18 Million Americans Could Lose Current Healthcare Plans Due To Obamacare

CBS: Obamacare Forcing Hundreds of Thousands to Lose Insurance Coverage

CBS: ObamaCare Enrollment Numbers Well Below Projections In Early Days

CBS: More than two million Americans being dropped from their insurance plans due to Obamacare

Obamacare and Other Lies…

Obama Officials In 2010: 93 Million Americans Will Be Unable To Keep Their Health Plans Under Obamacare

Avik Roy, Contributor

On Wednesday, Secretary of Health and Human Services Kathleen Sebelius testified before Congress about the continuing issues with the rollout of Obamacare’s health insurance exchanges. “Hold me accountable for the debacle,” said Sebelius. “I’m responsible.” I attended the hearing, and I was struck by the scope, scale, and depth of the health law’s problems, problems that far exceed any one political appointee. But Obamacare’s disruption of the existing health insurance market—a disruption codified in law, and known to the administration—is only just beginning. And it’s far broader than recent media coverage has implied.

Obama administration knew that Obamacare would disrupt private plans

If you read the Affordable Care Act when it was passed, you knew that it was dishonest for President Obama to claim that “if you like your plan, you can keep your plan,” as he did—and continues to do—on countless occasions. And we now know that the administration knew this all along. It turns out that in an obscure report buried in a June 2010 edition of the Federal Register, administration officials predicted massive disruption of the private insurance market.

On Tuesday, White House spokesman Jay Carney attempted to minimize the disruption issue, arguing that it only affected people who buy insurance on their own. “That’s the universe we’re talking about, 5 percent of the population,” said Carney. “In some of the coverage of this issue in the last several days, you would think that you were talking about 75 percent or 80 percent or 60 percent of the American population.” (5 percent of the population happens to be 15 million people, no small number, but let’s leave that aside.)

By “coverage of this issue,” Carney was referring to two articles. The first, by Chad Terhune of the Los Angeles Times, described a number of Californians who are seeing their existing plans terminated and replaced with much more expensive ones. “I was all for Obamacare until I found out I was paying for it,” said one.

The second article, by Lisa Myers and Hanna Rappleye of NBC News, unearthed the aforementioned commentary in the Federal Register, and cited “four sources deeply involved in the Affordable Care Act” as saying that “50 to 75 percent” of people who buy coverage on their own are likely to receive cancellation notices due to Obamacare.

Mid-range estimate: 51% of employer-sponsored plans will get canceled

But Carney’s dismissal of the media’s concerns was wrong, on several fronts. Contrary to the reporting of NBC, the administration’s commentary in the Federal Register did not only refer to the individual market, but also the market for employer-sponsored health insurance.

Section 1251 of the Affordable Care Act contains what’s called a “grandfather” provision that, in theory, allows people to keep their existing plans if they like them. But subsequent regulations from the Obama administration interpreted that provision so narrowly as to prevent most plans from gaining this protection.

“The Departments’ mid-range estimate is that 66 percent of small employer plans and 45 percent of large employer plans will relinquish their grandfather status by the end of 2013,” wrote the administration on page 34,552 of theRegister. All in all, more than half of employer-sponsored plans will lose their “grandfather status” and become illegal. According to the Congressional Budget Office, 156 million Americans—more than half the population—was covered by employer-sponsored insurance in 2013.

Another 25 million people, according to the CBO, have “nongroup and other” forms of insurance; that is to say, they participate in the market for individually-purchased insurance. In this market, the administration projected that “40 to 67 percent” of individually-purchased plans would lose their Obamacare-sanctioned “grandfather status” and become illegal, solely due to the fact that there is a high turnover of participants and insurance arrangements in this market. (Plans purchased after March 23, 2010 do not benefit from the “grandfather” clause.) The real turnover rate would be higher, because plans can lose their grandfather status for a number of other reasons.

How many people are exposed to these problems? 60 percent of Americans have private-sector health insurance—precisely the number that Jay Carney dismissed. As to the number of people facing cancellations, 51 percent of the employer-based market plus 53.5 percent of the non-group market (the middle of the administration’s range) amounts to 93 million Americans.

Will these canceled plans be replaced with better coverage?

President Obama’s famous promise that “you could keep your plan” was not some naïve error or accident. He, and his allies, knew that previous Democratic attempts at health reform had failed because Americans were happy with the coverage they had, and opposed efforts to change the existing system.

Now, supporters of the law are offering a different argument. “We didn’t really mean it when we said you could keep your plan,” they say, “but it doesn’t matter, because the coverage you’re going to get under Obamacare will be better than the coverage you had before.”

But that’s not true. Obamacare forces insurers to offer services that most Americans don’t need, don’t want, and won’t use, for a higher price. Bob Laszewski, in arevealing blog post, wrote about the cancellation of his own health coverage. “Right now,” he wrote, “I have ‘Cadillac’ health insurance. I can access every provider in the national Blue Cross network—about every doc and hospital in America—without a referral and without higher deductibles and co-pays.”

But his plan is being canceled. His new, Obamacare-compatible plan has a $500 higher deductible, and a narrower physician and hospital network that restricts out-of-town providers. And yet it costs 66 percent more than his current plan. “Mr. President,” he writes, “I really like my health plan and I would like to keep it. Can you help me out here?”

Congress proposes a straightforward solution

Senator Ron Johnson (R., Wisc.) and Rep. Fred Upton (R., Mich.) have proposed the “If You Like Your Health Care Plan You Can Keep It Act,” with dozens of co-sponsors. The two-page bill simply states that “nothing in [the Affordable Care Act] shall be construed to require that an individual terminate coverage under a group health plan or health insurance coverage in which such individual was enrolled during any part of the period beginning on the date of enactment of this Act and ending on December 31, 2013.”

Some Senate Democrats are jumping on the grandfathering bandwagon. Mary Landrieu (D., La.), locked in a competitive reelection race against Rep. Bill Cassidy (R., La.), now claims that she was unaware that Obamacare would disrupt existing insurance arrangements. “It was our understanding when we voted for that bill that people when they have insurance could keep with what they had. So I’m going to be working on that fix,” she said on Wednesday.

But that’s not accurate. It was well known, as far back as 2009, that millions of Americans would lose their existing coverage under the Obamacare bill. Landrieu still voted for it. In September of 2010, Sen. Mike Enzi (R., Wyo.) introduced legislation that would protect small businesses from losing their health plans’ grandfathered status under Obamacare. Landrieu voted against the bill, on a party-line vote.

But Landrieu’s flip-flop illustrates the potency of this issue. If Americans were truly being forced off of their existing insurance plans—that they like—and into better and more affordable ones, the outcry would be minimal. But that isn’t what’s happening. People are being forced into inferior and costlier plans. And they’re making their displeasure felt in Washington.

Expert: At least 129 million will ‘not be able to keep’ health care plan if Obamacare fully implemented

If Obamacare is fully implemented, 68 percent of Americans with private health insurance will not be able to keep their plan, according to health care economist Christopher Conover.

Conover is a research scholar in the Center for Health Policy & Inequalities Research at Duke University and an adjunct scholar at the American Enterprise Institute. In an interview with The Daily Caller, he laid out what he estimates the consequences of Obamacare’s implementation will ultimately be.

“Bottom line: of the 189 million Americans with private health insurance coverage, I estimate that if Obamacare is fully implemented, at least 129 million (68 percent) will not be able to keep their previous health care plan either because they already have lost or will lose that coverage by the end of 2014,” he said in an email. ”But of these, ‘only’ the 18 to 50 million will literally lose coverage, i.e., have their plans entirely taken away. This includes 9.2-15.4 million in the non-group market and 9-35 million in the employer-based market. The rest will retain their old plans but have to pay higher rates for Obamacare-mandated bells and whistles.”

for Obamacare-mandated bells and whistles.”

Conover also says it is hard to imagine President Obama didn’t know these statistics when he was flacking for his health care bill by promising Americans they could keep their health insurance if they liked it.

“If President Obama himself believed this the first time he said it, he was poorly advised,” Conover said.

“The problem is that he said it at least 24 times, most of which occurred after his own rule-writers had estimated that 49-80 percent of small employer plans would have lost their grandfather status by 2013, along with 34-64 percent of large employer plans. The same rule estimated that each year 40 to 67 percent of non-group plans not already grandfathered would lose their grandfather status. Given how extensively presidential statements — especially to a joint session of Congress — are vetted and fact-checked, it is pretty inconceivable that President Obama was not aware that he was engaged in some degree of truth-twisting.”

See TheDC’s full interview with Conover below:

Absolutely not. Technically, every single health plan in the country already has been subject to at least some new Obamacare requirements. That is, even “grandfathered” plans and self-insured plans were required to eliminate lifetime and annual limits and to cover dependents up to age 26 on their parent’s plan. Each of these “improvements” in coverage costs money, just as every feature you add to your car costs money (anti-lock brakes, all-wheel drive). For instance, an Aon Hewitt survey of insurers showed that expanding dependent coverage to age 26 could increase premiums by 1 percent for some in the large group market, 2 percent in the small group market and up to 3.5 percent in the non-group market.

So strictly speaking, NO ONE who was entirely satisfied with their pre-Obamacare coverage has been able to keep it. But the degree of new restrictions/added costs is a continuum, with the added requirements/costs imposed in the following order (starting with plans facing the least added restrictions):

· Grandfathered plans (in theory, any plan in the large group, small group and non-group market can be grandfathered, but the restrictions are so tight that eventually every plan is expected to lose grandfather status)

· Self-insured plans (most of these are large employers with at least 100 workers)

· Large employer plans that are not self-insured (for now, small group only includes those under 50 workers, but this will grow to under 100 workers by 2016 and states have option to expand the definition further in future years)

· Non-group plans (inside and outside Exchanges)

· Small group plans (inside and outside Exchanges)

Thus, the degree to which you are dissatisfied with the new restrictions imposed by Obamacare or adversely affected by higher premiums depends heavily on what type of coverage you currently have.

By your calculations, how many people could lose their health insurance plans as result of Obamacare’s implementation?

The plans that come closest to conforming to the president’s original promise are grandfathered plans. But most Americans are not in grandfathered health plans anymore:

· Only 30 percent of large firm workers are in grandfathered plans in 2013, meaning the other 70 percent have already had to upgrade to more expensive policies covering, for example, all preventive services without any cost sharing

· Similarly, only 52 percent of covered workers in small group plans are in grandfathered plans.

· It is estimated that 85 percent of non-group plans cannot qualify for grandfather status.

Bottom line: of the 189 million Americans with private health insurance coverage, I estimate that if Obamacare is fully implemented, at least 129 million (68 percent) will not be able to keep their previous health care plan either because they already have or will lose that coverage by the end of 2014. This includes:

· 9.2 to 15.4 million in the non-group market

· 16.6 million in the small group market

· 102.7 million in the large group market

But of these, “only” the 18 to 50 million will literally lose coverage, i.e., have their plans entirely taken away. This includes 9.2-15.4 million in the non-group market and 9-35 million in the employer-based market. The rest will retain their old plans but have to pay higher rates for Obamacare-mandated bells and whistles. It’s worth noting that RAND Corporation estimates that 3.8 million of these plan losers will not be able to find affordable coverage and will end up becoming newly uninsured.

Obama administration officials now say that those losing their insurance plans are actually losing inadequate coverage and that the new coverage they will be forced to get will be better and often cheaper. What do you say to that claim?

Here’s the problem: for additional coverage to be “better,” it must be worth the added cost from the perspective of the buyer. Prior to March 2010, there was nothing stopping employers or individuals from adding these benefit enhancements voluntarily, and indeed, many did. But tens of millions of others concluded that it wasn’t worth the added premium cost to extend dependent coverage from age 21 to age 26, for example, or to completely eliminate an already generous lifetime cap on benefits (e.g., $2 million). Obamacare essentially says “Uncle Sam knows best” by letting the judgment of government experts and bureaucrats trump that of American citizens, who used to have the freedom to make their own choices on these matters.

It’s true that some Americans will end up with cheaper coverage, but not the vast majority. Study after study shows premiums on average will be higher in the non-group, small group and even large group markets:

The Society of Actuaries predicts premiums will rise 31.5 percent on average in the non-group market.

· Heritage Foundation found that average premiums for a family

· American Action Forum (headed by former CBO director Douglas Holtz-Eakin) estimates that premiums for healthy 30-year-olds in the non-group market will increase in all fifty states and the District of Columbia – from a low of 9 percent in Massachusetts

· Even for 40-year-olds, Manhattan Institute estimates that premiums in the non-group market will increase an average of 99 percent for men and 62 percent for women.

These studies do not account for Exchange subsidies; however two studies have addressed this issue directly:

· In a state-by-state analysis, Manhattan Institute calculated the “break-even” income level needed to ensure that an individual’s subsidies would entirely offset the full estimated increase in premiums they would face in their home state. Both for 27-year olds and 40-year olds (whether male or female), the break-even income was well below median household income. Since by definition half of households are below the median, this result implies that a majority of individuals in the non-group market will pay higher premiums even after accounting

· National Journal’s independent assessment concluded that even after taking into account subsidies available on the exchanges, 66 percent of workers with single coverage and 57 percent of workers with family coverage will face higher premiums on the exchange compared to what they would pay for employer-sponsored coverage. The analysis showed that a single wage earner must make less than $20,000 to see his or her current premiums drop or stay the same under Obamacare. For a family of four, income would have to be less than or equal to $62,300 in order to see net premium savings

Is it possible President Obama truly believed his “if you like your health insurance, you can keep it” promise at the time he was saying it? Or were the consequences of Obamacare so foreseeable that such a scenario is hard to imagine?

If President Obama himself believed this the first time he said he, he was poorly advised. The problem is that he said it at least 24 times, most of which occurred after his own rule-writers had estimated that 49-80 percent of small employer plans would have lost their grandfather status by 2013, along with 34-64 percent of large employer plans. The same rule estimated that each year 40 to 67 percent of non-group plans not already grandfathered would lose their grandfather status. Given how extensively presidential statements — especially to a joint session of Congress — are vetted and fact-checked, it is pretty inconceivable that President Obama was not aware that he was engaged in some degree of truth-twisting. How much truth-twisting? Well, the Washington Post’s Fact-Checker, Glenn Kessler, has awarded the president Four Pinocchios for his pledge. That sounds about right to me.

What do you believe will happen if the Obamacare exchanges fail to sign up the needed percentage of the young and healthy? How serious a problem will that be?

There are mechanisms in place to protect individual health plans against ending up with an unexpectedly high selection of poor health risks. Nevertheless, if this phenomenon is occurring market-wide, it will result in substantially more taxpayer subsidies on the exchanges. Moreover, this adverse experience is likely to greatly influence decisions by health plans whether to re-participate in Year 2 (not to mention the companies that wisely sat out the first year so they could get a more accurate handle on the cross-section of health risks they would face so that they could more accurately price their products). Year 1 already suffers from pretty poor health plan participation (only 2 carriers offer coverage in North Carolina’s exchange, for example, even though there’s a half dozen carriers that previously offered plans in the non-group market). But this will make the exchanges even less desirable except for those heavily in need of subsidies (sicker/poorer). So I don’t think the death spiral will cause the immediate dissolution of the exchanges necessarily, but absent a change in the basic structure of Obamacare, I think it is close to inevitable.

Obamacare is a really bad deal for most young people. As one illustration, all the people who for many years used to be in 34 state high risk pools now will be channeled into the exchanges and the young are bearing the biggest burden of carrying this load (which previously used to be spread across all people with insurance and/or general taxpayers, depending on what state you lived in). As well, they are carrying the burden of paying for many older people who have much higher incomes. Young people only now are discovering this and I think it will become even more obvious this coming year. As young people discover how easy it is to evade the individual mandate penalty — i.e., make sure you don’t have a tax refund due and you’re home free — non-compliance is likely to increase rather than decrease over time even though the penalty itself will keep going up between now and 2016.

This interview has been edited for clarity and brevity.

Stage 4 Cancer – Lung, Liver, and Gallbladder Surgery – My 6 Year Journey

You Also Can’t Keep Your Doctor

I had great cancer doctors and health insurance. My plan

By

Everyone now is clamoring about Affordable Care Act winners and losers. I am one of the losers.

My grievance is not political; all my energies are directed to enjoying life and staying alive, and I have no time for politics. For almost seven years I have fought and survived stage-4 gallbladder cancer, with a five-year survival rate of less than 2% after diagnosis. I am a determined fighter and extremely lucky. But this luck may have just run out: My affordable, lifesaving medical insurance policy has been canceled effective Dec. 31.

My choice is to get coverage through the government health exchange and lose access to my cancer doctors, or pay much more for insurance outside the exchange (the quotes average 40% to 50% more) for the privilege of starting over with an unfamiliar insurance company and impaired benefits.

Countless hours searching for non-exchange plans have uncovered nothing that compares well with my existing coverage. But the greatest source of frustration is Covered California, the state’sAffordable Care Act health-insurance exchange and, by some reports, one of the best such exchanges in the country. After four weeks of researching plans on the website, talking directly to government exchange counselors, insurance companies and medical providers, my insurance broker and I are as confused as ever. Time is running out and we still don’t have a clue how to best proceed.

Two things have been essential in my fight to survive stage-4 cancer. The first are doctors and health teams in California and Texas: at the medical center of the University of California, San Diego, and its Moores Cancer Center; Stanford University’s Cancer Institute; and the M.D. Anderson Cancer Center in Houston.

The second element essential to my fight is a United Healthcare PPO (preferred provider organization) health-insurance policy.

Since March 2007 United Healthcare has paid $1.2 million to help keep me alive, and it has never once questioned any treatment or procedure recommended by my medical team. The company pays a fair price to the doctors and hospitals, on time, and is responsive to the emergency treatment requirements of late-stage cancer. Its caring people in the claims office have been readily available to talk to me and my providers.

But in January, United Healthcare sent me a letter announcing that they were pulling out of the individual California market. The company suggested I look to Covered California starting in October.

You would think it would be simple to find a health-exchange plan that allows me, living in San Diego, to continue to see my primary oncologist at Stanford University and my primary care doctors at the University of California, San Diego. Not so. UCSD has agreed to accept only one Covered California plan—a very restrictive Anthem EPO Plan. EPO stands for exclusive provider organization, which means the plan has a small network of doctors and facilities and no out-of-network coverage (as in a preferred-provider organization plan) except for emergencies. Stanford accepts an Anthem PPO plan but it is not available for purchase in San Diego (only Anthem HMO and EPO plans are available in San Diego).

So if I go with a health-exchange plan, I must choose between Stanford and UCSD. Stanford has kept me alive—but UCSD has provided emergency and local treatment support during wretched periods of this disease, and it is where my primary-care doctors are.

Before the Affordable Care Act, health-insurance policies could not be sold across state lines; now policies sold on the Affordable Care Act exchanges may not be offered across county lines.

What happened to the president’s promise, “You can keep your health plan”? Or to the promise that “You can keep your doctor”? Thanks to the law, I have been forced to give up a world-class health plan. The exchange would force me to give up a world-class physician.

For a cancer patient, medical coverage is a matter of life and death. Take away people’s ability to control their medical-coverage choices and they may die. I guess that’s a highly effective way to control medical costs. Perhaps that’s the point.

Ms. Sundby lives in California.

http://online.wsj.com/news/articles/SB10001424052702304527504579171710423780446

Read Full Post | Make a Comment ( None so far )

You must be logged in to post a comment.